Editor’s note: Bob Shullman is the CEO and founder of The Shullman Research Center, New York.

As you're reading this, the countdown to the holiday shopping season has already begun and store windows are preparing full Christmas/Hanukkah/Kwanzaa displays. However, behind the glitter, glitz and glamour of the merchandise displays is the hard fact that, for the vast majority of media, online retailers, brick-and-mortar stores, marketers and their agencies, the 2014 holiday season results generally determine success or failure for the entire year.

The latest Shullman Luxury, Affluence and Wealth Pulse* took a deep dive into how mass-market and affluent American adults (18+ in age) are planning to shop for the 2014 holidays. As part of this wave of our ongoing survey, we studied how upscale Americans (those who live in households with household incomes of $75,000 or more – the top 42 percent) are planning to shop for the holidays according to the generation to which they belong – Millennials, Generation X, Boomers and seniors.

Some might question why those with household incomes of $75,000 should be considered affluent, and to that I contend that such consumers – especially during the holiday season – often spend above their usual patterns.

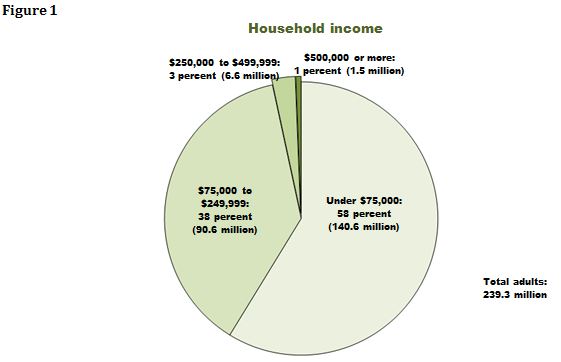

To better understand the size and scope of the 42 percent, Figure 1 illustrates the sizes of selected household income segments in the United States based on an estimated total adult population (18 years of age or older) of 239.3 million, according to the March 2014 current population survey from the U.S. Census Bureau, published in September 2014. In that regard, American adults with household incomes of less than $75,000 are now included in our findings.

Source: Bureau of the Census, March 2014 Current Population Survey

The overall good news is that most consumers plan to do holiday shopping this year, and many in the higher-income and wealthy segments have already (as early as August) started their shopping. At the same time (and this is a concern), 18 percent do not plan to do any holiday shopping, and their reasons for abstaining are diverse. For example (these are representative quotes from adults not planning to shop for the 2014 holidays):

"I don't believe in the holidays."

"I lost my job recently and don't have any money to spend."

"We get together with our family and enjoy the time, so we don't waste our money on buying holiday gifts."

A more hopeful answer (at least to retailers):

"My spouse does all the shopping in my house and I am not involved."

At the same time, while not abstaining from holiday shopping, 16 percent of all adults are planning to spend less this year, and the following quotes from such adults are illuminating:

"I don't feel good about what is going on in the world; it's time to save one's money."

"I recently wrote the first check for my child's college tuition."

"I need to replace our car soon, and can't afford to also buy holiday gifts."

"I'm concerned about losing my job."

"I'm unemployed."

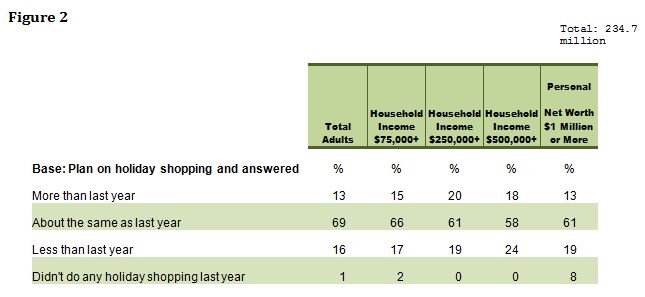

On the more positive side, the vast majority (69 percent, as shown in Figure 2) are planning to spend about the same as last year, while 13 percent are planning to spend more, as the following quotes explain:

"I recently received a raise."

"The economy is getting better and I am more optimistic about the future."

"I won a large amount in our state's lottery!"

"I switched jobs for more money and now have more money to spend."

As to where consumers will be shopping, online-only stores such as Amazon and eBay rule the roost, with 74 percent of those with household incomes of $500,000 or more planning to shop at such sites. Figure 3 shows that discount stores (a close second among total adults) are more popular among the average consumer than among upscale segments, while mainstream department stores and specialty stores attract more than half of those with household incomes of $250,000 or more. As expected, compared with the average consumer, upper-income and wealthy consumers are more likely to frequent luxury stores.

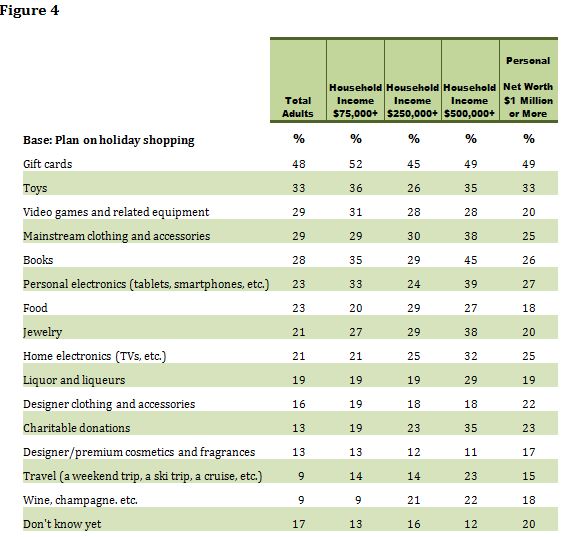

And what are they planning to buy? In something of a blow to wrapping paper and ribbons, gift cards came out at the top of the list for this holiday season among total adults and all the upscale segments, with 48 percent of all adults planning to give them this year (Figure 4). Perhaps that's a sign of today's stressful times, with people having less time and inclination to really shop. However, on the more traditional side, toys, video games, clothing/accessories and books remain popular gifts. On the more uplifting side, notably among those with household incomes of $500,000 or more, 35 percent plan on giving charitable donations. Finally, some 17 percent have not yet decided what to buy, which provides marketers with a great opportunity to influence their upcoming holiday shopping.

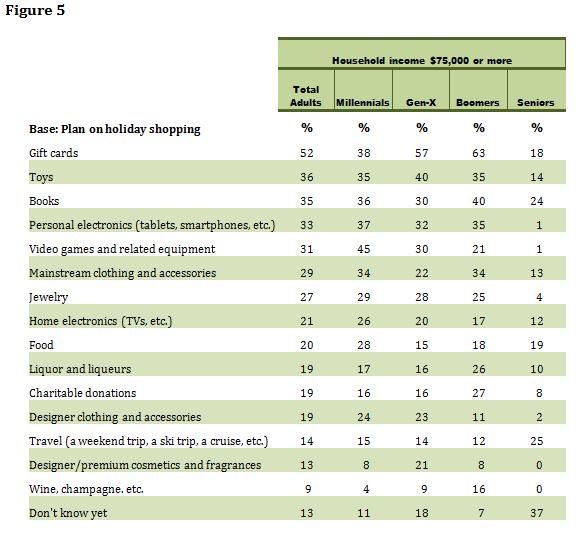

However, when it comes to such planned gifts, marketers must be aware that not all consumers are alike and one size does not fit all. Indeed, there are marked differences among the generations, so marketing plans should be geared accordingly. For example, Figure 5 details the most popular gift among each generation: upscale Millennials are planning to purchase video games and related equipment (45 percent); among seniors, it is travel (25 percent) and books (24 percent). Interestingly, some 27 percent of Boomers plan to make charitable donations, and 37 percent of seniors are still thinking about what to give.

So, now that we know the who, what, where and why, the next issue is "how much." Here too the generational differences apply, since upscale Millennials and Boomers are planning to spend more this year (over $1,500 on average) compared with Gen-X and seniors, with planned spending ranges from about $1,000 to $1,100 on average (Figure 6).

The 2014 holiday season will likely be a time of challenge and opportunity to the marketing community, especially those in the affluent spaces, with no dramatic rise or fall in planned consumer expenditures. I say challenge because there is no single way to address this market, so the opportunity lies in how to understand the generational differences and turn those into sales.

*The insights and data presented in this article are based on the Shullman Luxury, Affluence and Wealth Pulse, fall 2014 wave, conducted online between August 22 and August 27, 2014, among adults age 18 or older. Five sample groups of 1,665 respondents were surveyed that included a representative national sample of adults (1,003 interviews), plus four household-income segments that were targeted to obtain the following number of completed interviews, resulting in a total of 1,056 interviews among upscale consumers with household incomes of at least $75,000:

$75,000 to $149,999: 303 interviews

$150,000 to $249,999: 250 interviews

$250,000 to $499,999: 251 interviews

$500,000 or more: 252 interviews

Additionally, 497 respondents in this survey wave reported that their net worth was $1,000,000 or more and have been classified as millionaires.

Survey results were weighted on demographic characteristics to reflect estimates from the March 2013 Current Population Survey of the Bureau of the Census released in September 2013.