Editor’s note: Richard Snoxell is a research director in the tech and financial team at U.K.-based market research agency, Marketing Sciences Unlimited. This is an edited version of a post that originally appeared here under the title, “For customers, the real draw of mobile wallet is … not mobile payments.”

We have been closely monitoring U.K. consumer sentiment toward mobile wallet on a quarterly basis for 18 months now as the disruptions in the financial tech sector gather pace. As addition to brand trust, in this blog we also take a look at the features which would drive consumer uptake of wallet – and it’s still not mobile payments.

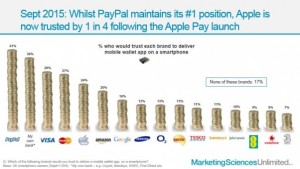

More on that later; let’s start by looking at brand trust. We see that PayPal continues to maintain a trust figure around the 40 percent mark. This is unchanged over 15 months and is partly thanks to its heritage in this sector, and users feeling reassured by the way PayPal places a buffer between a user’s bank details and the recipient. There has also been consistency in second place for “my own bank” (nobody likes bankers but most still trust their own bank), with Visa and MasterCard in third and fourth place, respectively. However, the one brand we have seen consistent upwards movement with is Apple.

More on that later; let’s start by looking at brand trust. We see that PayPal continues to maintain a trust figure around the 40 percent mark. This is unchanged over 15 months and is partly thanks to its heritage in this sector, and users feeling reassured by the way PayPal places a buffer between a user’s bank details and the recipient. There has also been consistency in second place for “my own bank” (nobody likes bankers but most still trust their own bank), with Visa and MasterCard in third and fourth place, respectively. However, the one brand we have seen consistent upwards movement with is Apple.

Apple Pay launched in the U.K. in July 2015 but it has taken several months for the Apple logo to start appearing on a significant number of contactless payment terminals in retailers; and personally I haven’t heard staff promoting it yet – but that’s understandable as so few people have an iPhone 6 or 6s (and staff would have to spot that too). However, the release of the iPhone 6s has coincided with increased Apple Pay advertising by financial institutions and retailers in the long pre-Christmas push so it will come more to mind as we move into 2016.

The impact of this has been a slow but steady improvement in brand trust for Apple as it begins to make its mark in the sector. Trust in Apple has increased from 18 percent in May 2014 to 24 percent in September 2015.

In that same period Samsung has hovered around the 12-to-13 percent mark. Compared to iPhone owners, users of Samsung mobiles tend to be less evangelical about its products and on average slightly less techy. Also, Samsung owners who are interested in mobile wallet will also soon need to decide whether to throw their financial eggs into a Samsung Pay or Android Pay basket, a choice that iPhone users do not have to make. Despite the fact that Samsung Pay will be potentially usable in more outlets thanks to its support of the older magnetic stripe payment technology (in addition to contactless), I expect improvements in Samsung’s trust rating will be harder to come by, even if Samsung Pay is a hit. Both services are expected to launch in the U.K. in the coming months but no dates have been announced yet.

Digitizing loyalty cards and vouchers will drive uptake

The features in a mobile wallet app that will drive uptake will be genuine value-add services that consumers don’t currently have – the ability to digitize your physical loyalty cards and vouchers and so save space – and never forget to use them. This trumps by some way the convenience of mobile payments in a physical store environment. As part of the iOS 9 release for the iPhone 6 and 6s in September, Apple Passbook has been revamped as Apple Wallet, additionally bringing in the non-payment features as described above to users. This latest version of the software has also made the biometric fingerprint sensor on the iPhone 6 and 6s twice as fast as before.

However, as discussed previously, it may be in-app purchasing that truly drives uptake of Apple Pay, by speeding up online purchasing and removing the need to log in to your account at each retailer (and remember each password).

What is also interesting is looking at the jump in the contactless payment limit from £20 to £30, and comparing this to a scenario where this artificial limit is removed. There is a tiny bit more reticence in making a £30 payment than a £20 one but there appears to be a committed group of around one fifth of users (21 percent) who are simply comfortable with the idea of using their smartphone for a contactless payment just like they would with their plastic payment card.

Finally it’s also worth noting that smartwatches will definitely play an important role in the future of mobile payments. Around one in 10 of those surveyed said they would use a watch rather than a phone for payments, if they owned both. This rises to 15 percent of 25-to-34-year-olds. One of the advantages of a watch is that once on the wrist and paired with the smartphone (in the morning, say) it is then ready to use for the rest of the day until removed from the wrist – unlike the smartphone which usually has to be securely unlocked each time. Now that’s genuinely convenient.