Editor's note: Richard J. LaRosa is associate professor at California University of Pennsylvania, California, Pa. Brian F. Blake is professor emeritus, consumer-industrial research program at Cleveland State University. Yang Luming is professor, e-commerce department, Yunnan University, China. Kimberly A. Neuendorf is professor, school of communication, Cleveland State University. Karen Hudzinski is analyst, consumer insights and strategy at Macy’s Inc.

The marketer’s world is exploding! Not just in the U.S. but globally as well. Seemingly overnight, consumers are now shopping with new electronic devices like credit-card readers or price-comparison mobile apps. They use new vehicles like digital media stores. They seek information from new sources like vlog review sites. They buy new types of products like e-gift cards. Marketers are scrambling to capitalize on the new opportunities presented, while investigators try to grasp the dynamics of the new shopping landscape. It is an exciting, though daunting, time for marketing researchers.

More and more, clients with e-tail operations want marketing researchers to provide a broad picture of the e-marketplace and the client’s position in it. Among other issues, clients are asking: Through which e-channels do shoppers find out about my products/services? What tools do consumers use to shop online? What new e-vehicles can I potentially use to effectively distribute my products? Answering these questions is far from a slam dunk.

First, for us to systematically research our clients’ questions, we need a clear delineation of the alternative vehicles now available to consumers to do their shopping. The classification must be comprehensive but reasonably brief.

Second, to devise such a classification, though, we must first start with a clear idea of what is and what is not e-shopping in the current global market. Consider Mary. She is thinking of buying a new kitchen blender, so she asks her Facebook friends what they think of the brands she is considering. Tony is choosing a restaurant for an impromptu dinner with his girlfriend and uses his smartphone to choose a nearby place offering a good coupon. Aren’t these just two examples of newer forms of shopping that should be included, along with distributors’ sites and other more “traditional” forms of online shopping? To work for a researcher, the definition must be up to date. It must cover the various shopper behaviors and the different sites or sources of the information/products that exist in the new market reality.

Third, we need hard data to determine which tools are viable communication vehicles for our client in a given target market.

To provide the needed framework, our research team has launched a multifaceted investigation of those consumers in the vanguard of these revolutionary changes. These are the young, educated Millennials in the world’s two largest e-shopping markets: the U.S. and China.

Virtual or tangible

So, how do we define e-shopping? As proposed elsewhere (Blake, LaRosa, Yang, Skalski, Neuendorf and Wu, 2012), e-shopping can be a consumer’s primary goal or can occur when a consumer is focusing principally upon other goals (e.g., socializing). So, it occurs not only on sites dedicated to sales/marketing but also on sites focused upon other objectives. Further, it can involve acquiring information intentionally or unintentionally and consumption in virtual or tangible form.

Six different forms of e-shopping behavior, then, are possible:

- Intentional information acquisition, e.g., browsing for product information via search engines

- Incidental information acquisition, e.g., learning options available on a BMW when playing Gran Turismo

- Selecting products for offline consumption, e.g., choosing an auto tire

- Selecting products for virtual consumption, e.g., choosing music files

- Virtually consuming products, e.g., listening to music

- Using a digital purchase device, e.g., apps for purchasing pizza

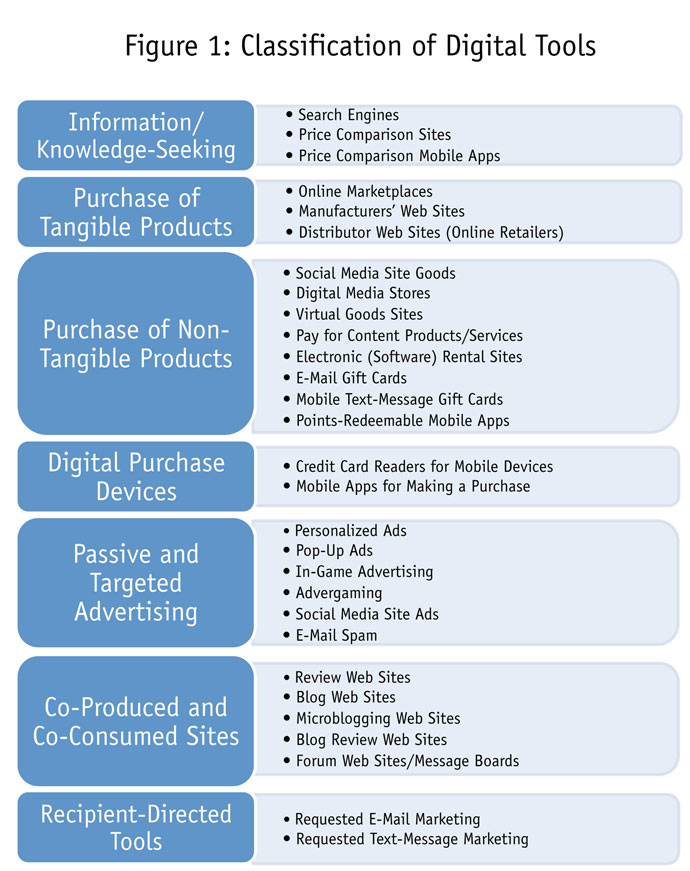

These behaviors are supported through the e-shopping tools presented in Figure 1.

The advent of e-tools has significantly broadened the context of product and service shopping. By far, most instances of e-shopping involve five site sources:

- sales/marketing organizations, e.g., manufacturers, distributors, political parties involving “traditional” B2C commerce;

- other consumers overtly engaging in C2C selling, e.g., selling an item on eBay;

- third-party information sources, e.g., bloggers, price aggregators;

- other persons not overtly selling, e.g., friends complaining about a product on a social media site;

- intruders into sites of other sources, e.g., pop-up ads on a news site.

To be useful to researchers, a vehicle classification must accommodate all six forms of shopping behavior and all five site sources.

The data

In the last two years, an online survey in the U.S. recruited 323 Millennials (18-34), students at two large and one smaller university in the east and midwest. The 776 young Millennials in China were students at one large and three small southwestern schools. Respondents were young; 98 percent of the U.S. and 99 percent of the China samples were 18-25. Though these samples are not strictly representative of their respective nations, they certainly can provide the useful point of departure we need.

The questionnaire described 28 different shopping vehicles. For 22 vehicles, respondents indicated whether they “never heard,” “heard but unfamiliar,” “familiar but never used” or “used at least once or twice.” These measures, however, were not relevant for the six tools in the passive and targeted advertising category.

Classification and results

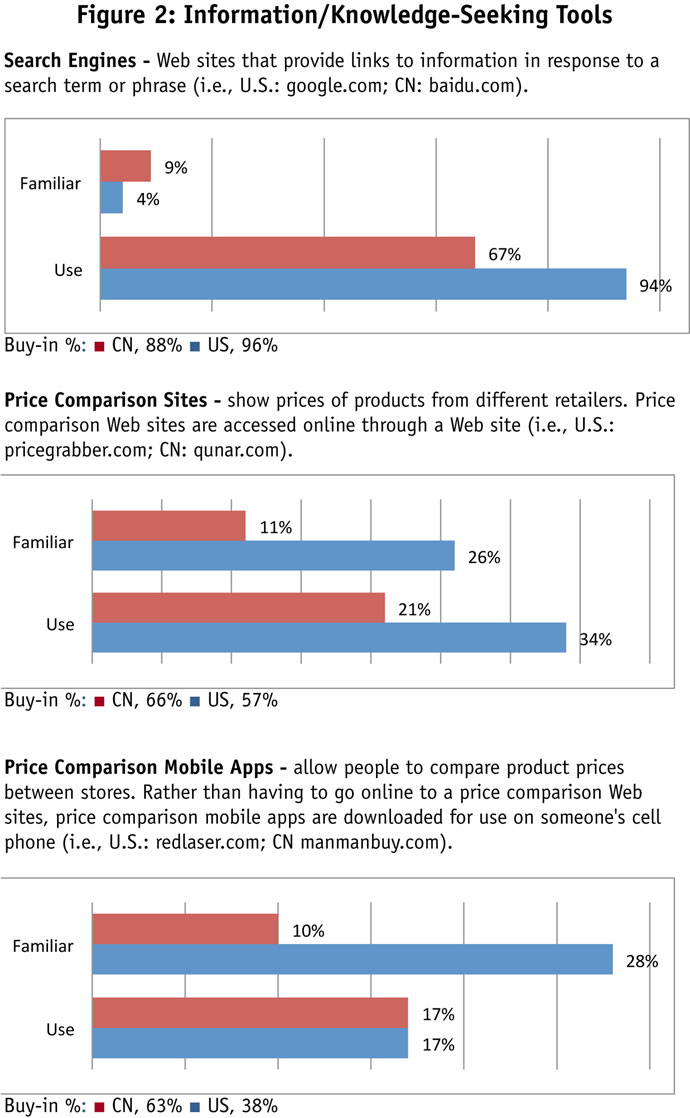

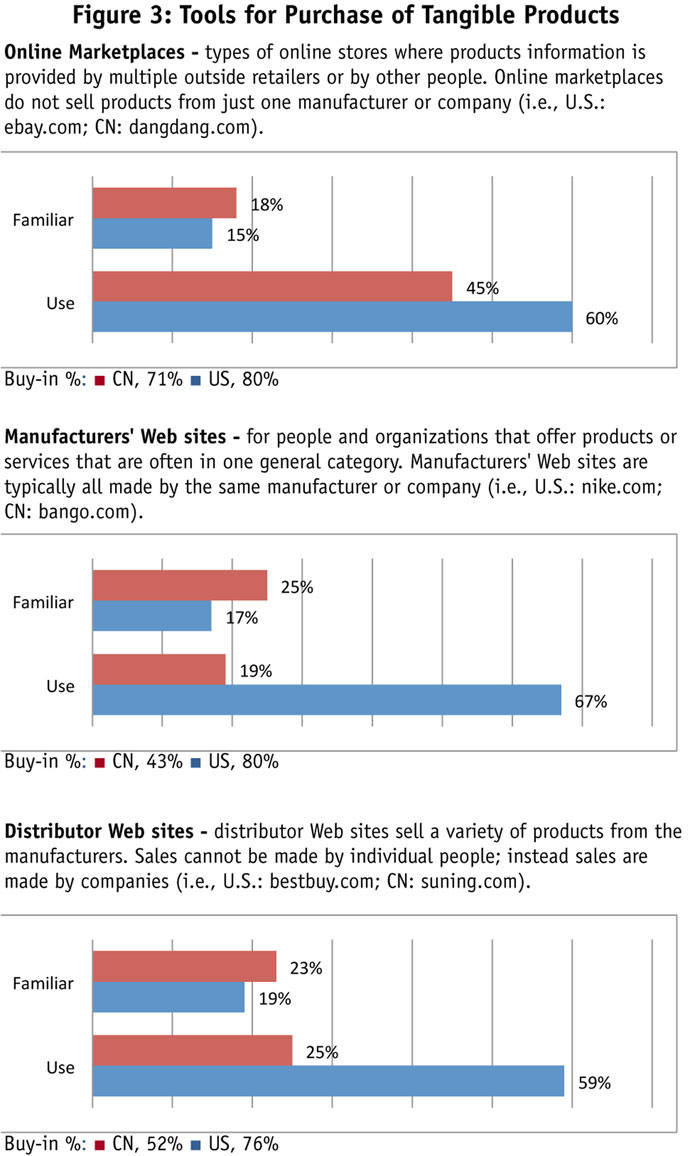

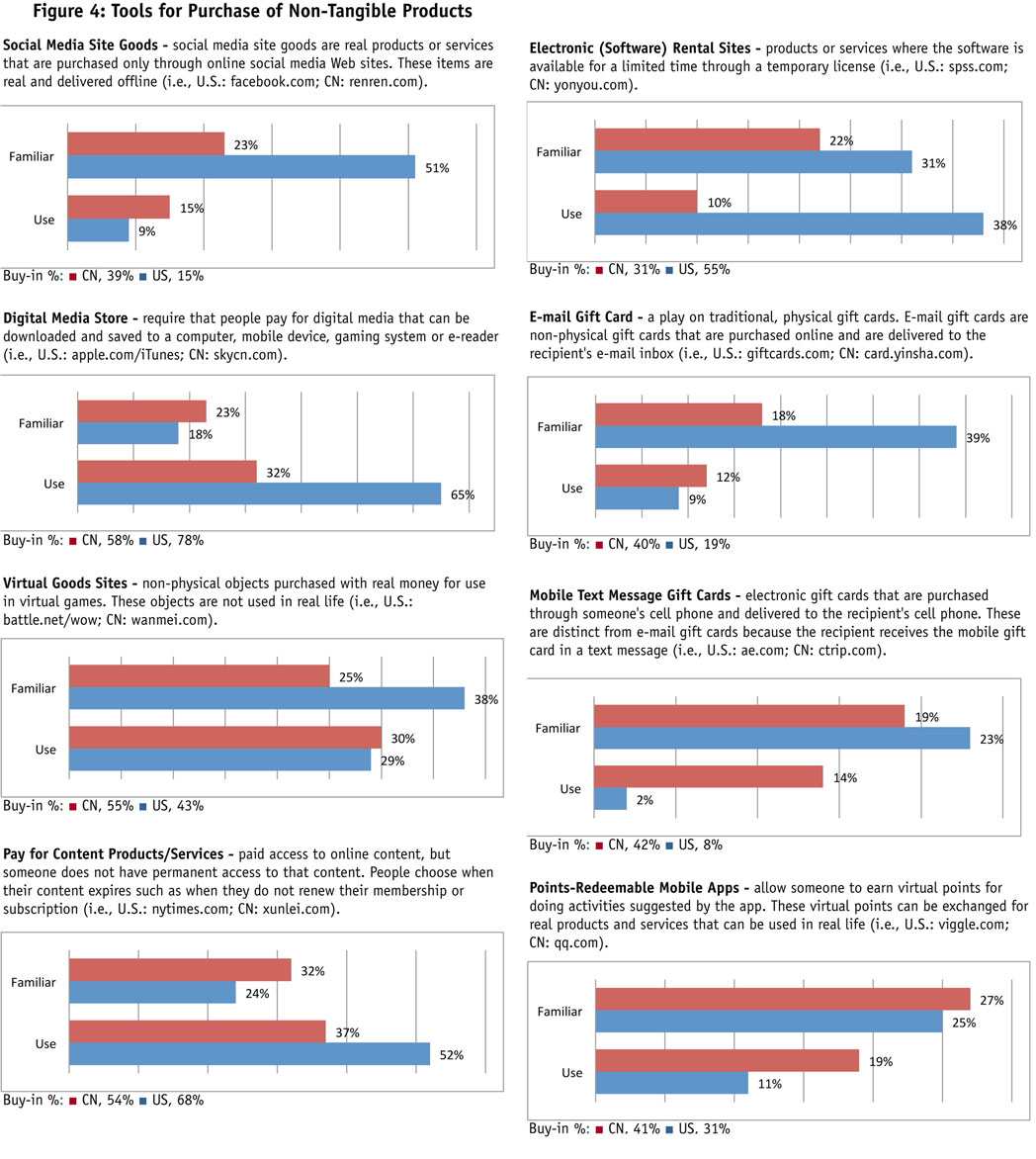

The 22 vehicles are described below. For each we present the percentage of the samples indicating they were familiar (but not used) and use (at least once or twice).

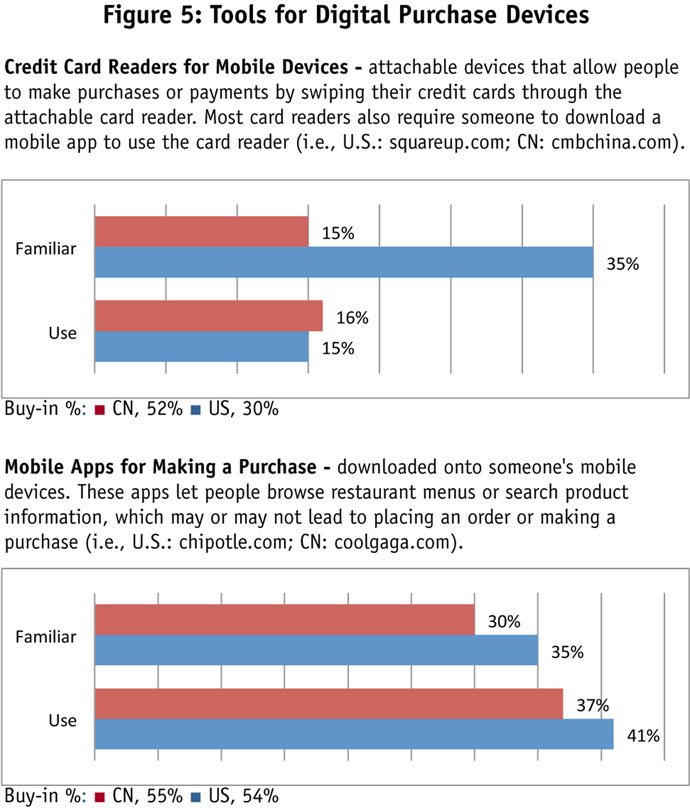

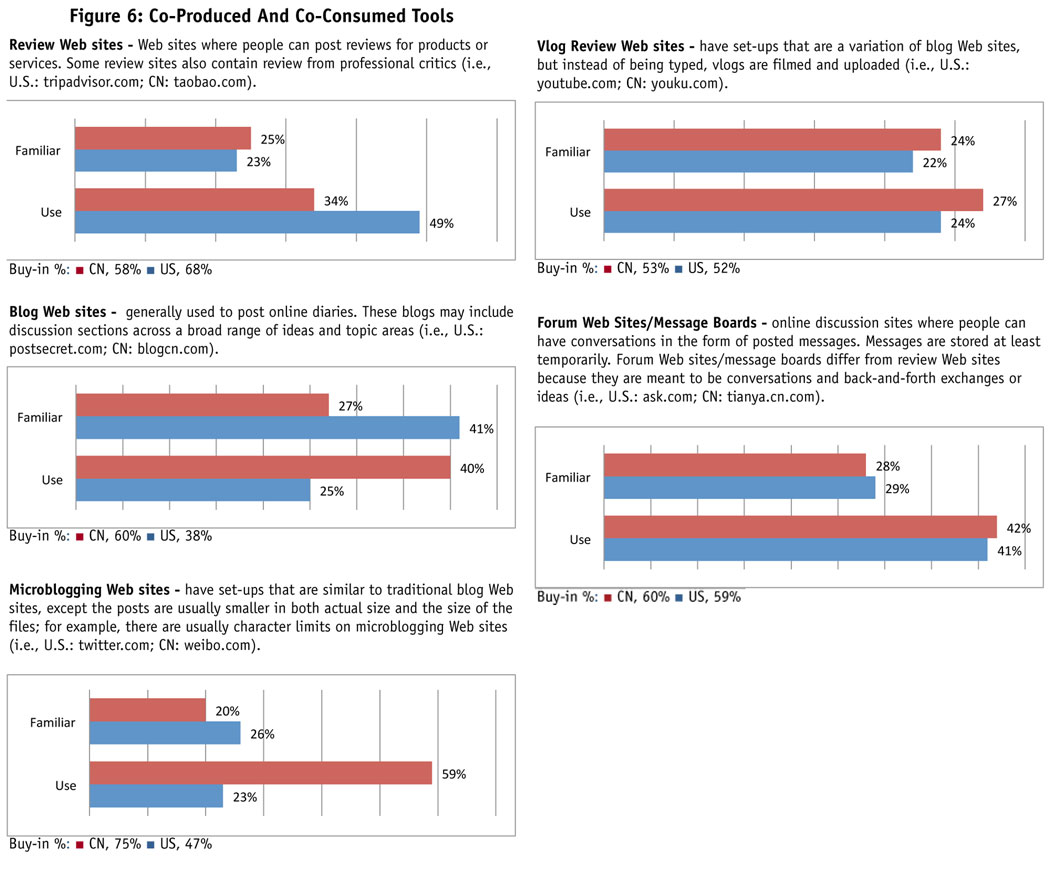

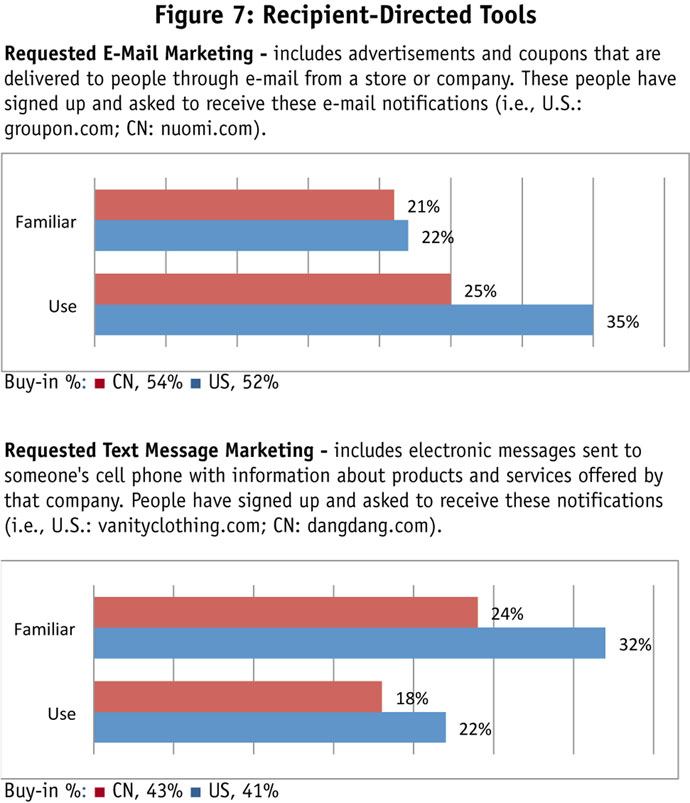

In the bar graphs China is red and the U.S. is blue.

Below each bar graph is a buy-in score. This is a rough gauge of how much a vehicle is described by the old observation “To know ’em is to love ’em.” It is the percent of those respondents familiar with a vehicle that has chosen to try it at least once or twice. Naturally, before a firm devises an integrated marketing program, it should know more than the current usage of shopping vehicles in the target market. It would also be valuable if the firm would have some insight into how those current rates might shift. We suggest that the buy-in score helps raise a few flags in this regard.

Specifically, if a vehicle has achieved little familiarity as yet in a market but has strong buy-in, we anticipate that usage may well become more widespread as familiarity with the new vehicles spreads. We might label this as a “potential breakout vehicle.” Conversely, if a vehicle’s familiarity is widespread but usage is low, we might call it a “potential flopper.” Illustrated by a firm’s sending unsolicited print ads to home or office fax machines, it may be a vehicle out of step with current technology or target shopper lifestyles.

Again, the buy-in percent for China is red and for the U.S. is blue.

Search engines (Figure 2) now have high usage, especially in the U.S. Buy-in is high in both nations. Price-comparison mobile apps are not popular as yet; they but may be headed toward a breakout in China, though not so in the U.S.

Manufacturer Web sites are shaky in the Chinese sample, with modest current usage and modest buy-in (Figure 3). Distributor sites are fairly similar in this regard. For online marketplaces, on the other hand, usage is substantial, particularly in the U.S., with strong buy-in in both markets.

Social media site goods differ dramatically from digital media stores (Figure 4). In the U.S., social media site goods, with considerably higher familiarity than usage, show indications of flopping. In contrast, in the U.S. social media stores are strong now and have good buy-in. Further, in the U.S. digital media stores may be ready for a breakout. The value of virtual site goods, though, is more tenuous. In China, social media site goods, digital media stores, and virtual goods sites are moderately healthy.

Pay-for-content vehicles display good current usage and even better potential in the U.S. This is true to a lesser degree in China. On the other hand, in the U.S., sample e-mail gift cards and text message gift cards look weak now and perhaps may weaken further among U.S. Millennials.

Generally, the U.S. and Chinese patterns are distinctive.

Credit card readers for mobile devices (Figure 5) enjoy only modest current usage in the U.S. and China. Buy-in scores, though, suggest that usage by Millennials may grow as awareness improves in China. This growth may not be as likely in the U.S. Mobile apps for making a purchase enjoy moderate health in both national samples.

In China, blog and microblog sites are strong now and offer evidence of becoming stronger (Figure 6). Such strength is not as evident in the U.S. In both Millennial groups, review site and forums/message boards are used often and have positive buy-in.

Requested e-mail and requested text-message marketing offer marketers potential in both Millennial samples (Figure 7).

Recommendations

First, we researchers should consider the vehicle classification offered here. It is quite inclusive, current and incorporates all six shopping behaviors and five site sources. It usefully flags for marketers some of the less obvious means by which consumers learn about and obtain their products. The classification can, then, serve as a heuristic, suggesting currently unused vehicles marketers can employ in a well-integrated marketing campaign.

Second, as researchers we should not base our analyses and recommendations on the assumption that Millennials are invariably in the forefront of technological innovation. While this may or may not be true when we compare Millennials to other market sectors, the Millennials sampled here have not overwhelmingly turned to the newer vehicles as yet.

Third, be alert to the, at times, great differences between the world’s two largest e-commerce markets in their reactions to e-shopping vehicles. Figure 4 is particularly clear on this point.

Finally, best practices and rules of thumb cannot necessarily be generalized from one national market to the other, no matter how successful those ideas are in either market considered alone. It is our responsibility as researchers to identify what can and what cannot be generalized to other national markets.

REFERENCES

Blake, B.F., LaRosa, R., Yang, L., Skalski, P., Neuendorf, K. A., and Wu, M. (2013) “What constitutes consumer ‘e-shopping’? Behaviors and vehicles in the U.S. and China. National Social Science Technology Journal, 3 (1), 1-13.