‘In order to change direction, we must hit a wall first!’

Resilience is a something we’ve all had to exhibit lately, as the pandemic and its associated effects impact us in ways that seem to constantly change. Beyond the chaos visited upon our day-to-day existences, our professional lives have been upended. Most of us are now working from home, engaging with customers, colleagues and friends over Zoom calls. Sometimes that’s great. Other times it sucks. But, thanks to resilience, somehow we’re managing. That which does not kill us, right?

Researchers are doing better than just managing, according to findings from our annual Q Report survey of client-side insights professionals. And while it would be an overstatement to say they are thriving, in reply after reply to the many open-ends we asked in this year’s iteration of the survey, they expressed optimism, pride, excitement and almost a sense of renewal even in the face of a worldwide disaster.

Recognizing 2020’s unique circumstances, we scrapped our usual approach for this year’s Q Report survey, replacing questions about salary and compensation and other aspects of life as a researcher with a focus on life as a researcher during a pandemic, with liberal use of open-ends to let respondents tell their stories in their own words.

The 2020 Q Report work life study of corporate researchers is based on data gathered from an invite-only online survey sent to pre-qualified marketing research end-client subscribers of Quirk’s. The survey was fielded from July 29 to August 12, 2020. In total we received 463 usable qualified responses. An interval (margin of error) of 4.5 at the 95 percent confidence level was achieved. (Not all respondents answered all questions.)

51 percent reported a cut in pay

We started the survey out by trying to get a handle on the pandemic’s impact on readers’ salary and work hours. Of the 100 responses we received to the question, “Which of the following apply to your employment since the COVID-19 crisis?” (my pay has been cut; I have been or am furloughed; my hours have been reduced), 51 percent reported a cut in pay; 34 percent said they have been or were currently furloughed; and 15 percent reported having their hours reduced. (Multiple responses were accepted.)

Next we asked about staffing levels and, perhaps surprisingly, 76% said their staffing levels have stayed the same. Just over 6% said the levels had increased and 17% said levels had been reduced through permanent job cuts, furloughs or hour reductions.

Those numbers were generally echoed in the range of comments on staffing. Hiring freezes were frequently cited. There were many mentions of being overworked and understaffed. Some departments had furloughs or forced vacation but are now coming back to full strength. There have been permanent reductions in staff along with a few staff expansions and multiple respondents wondered aloud about possible reductions to come later in the year if the virus’s effects linger.

To get more clarity on the hiring plans we asked how likely it was that the organization would hire additional MR employees in the next 12 months. Some variation of “unlikely” drew the highest percentages – 36% very unlikely; 17% unlikely and 6% somewhat unlikely – while the “likelys” as a group only mustered a collective 23%.

Related to staffing, of course, is budget and we asked how the budget or spend on MR had changed in 2020 due to COVID-19. About 45% said their budget had stayed the same. Just over 30% said their budget had decreased by more than 10%. Ten percent said they had seen a decrease of between 5% and 10%.

Of those who reported increases, 3% cited a budget rise of less than 5%, just under 4% cited an increase of between 5%-10% and just 2% enjoyed an increase of more than 10% in their insights budgets.

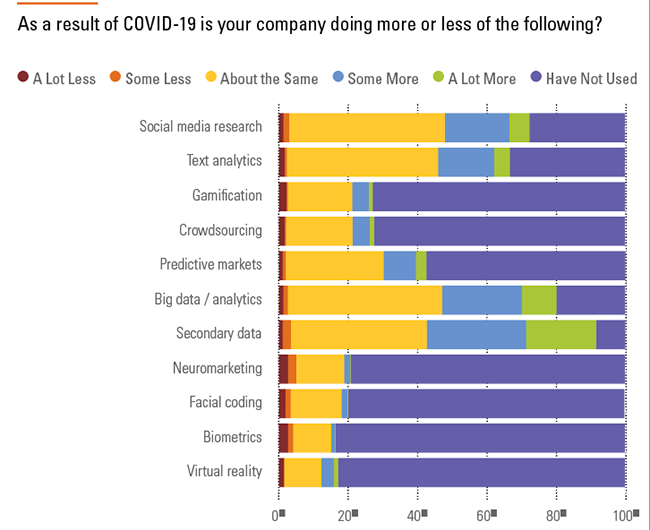

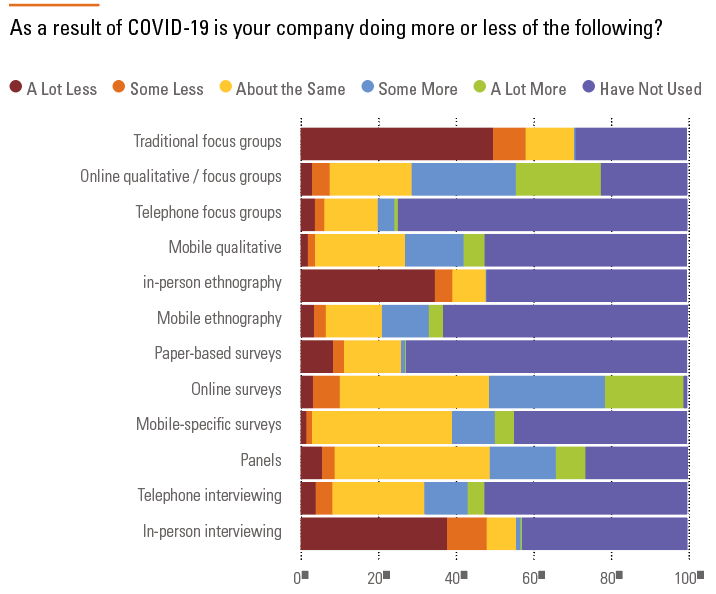

So, which techniques are those budgets being used on? We asked identically worded questions about two broad groupings of techniques (see accompanying charts). The first grouping encompassed techniques that are more widely or commonly in use. There, panels, online surveys and mobile-specific surveys scored the highest percentages of those reporting the same usage levels. And while traditional focus groups, at almost 50%, earned the highest “a lot less” usage percentages – along with in-person interviewing (38%) and in-person ethnography (35%) – online qualitative/focus groups earned a combined 47% “some more” or “a lot more” usage, so it’s clear that the problem lies with the in-person aspect of qual, not the techniques themselves.

In-person declines

Among the second grouping of techniques – generally those that are newer and/or less commonly used – secondary data earned the highest combined percentage (nearly 50%) of “some more” or “a lot more” usage, a finding that was borne out in several open-end comments. While the sheer volume of COVID-19 “reports” being issued by seemingly every research company in the world this spring took on its own virus-like aspects, apparently the onslaught was warranted, as our survey clearly showed a thirst for that kind of information among client-side researchers. Many respondents mentioned using the reports and other secondary sources to help get a big-picture handle on what was going on with the world in general and their consumers in particular.

I’ve gathered and synthesized more secondary research during the last few months than I have in years to help the organization better understand the state of the world and our industry.

There has been a lot more secondary research available and we’ve been using it!

Biggest change

We asked respondents to tell us in an open-end about the biggest change their organization has made related to marketing research as a result of COVID-19. The change could be anything but most responses centered around the tools and techniques that were – or were not – being used as much as before. As you would expect, in-person research basically stopped altogether in favor of digital and/or online equivalents. No focus groups, one-on-ones or CLTs.

We shifted all of our focus on studies that revolve around the impact of COVID-19. We tried operating as “business as usual” the third week of March when everything was shutting down but it was impossible to ignore how it has fundamentally changed how we go about our daily lives and impacted shopping behavior.

No in-person research is being conducted; otherwise we have continued with online surveys and online qualitative as before covid.

Our biggest change has been the shift from traditional, in-person, multi-city focus groups to online qualitative in its many forms. We’ve used OBBs, online groups, online one-on-ones ... anything that doesn’t require travel or the face-to-face meeting of our consumers is fair game right now.

Focus groups are now only online – interestingly, we are getting the same quality insights this way (cheaper and less travel for team members).

Moved away from extensive in-person playtest and usability tests and gone completely online. We are only now dipping our toe back into the water to try some very small in-person playtests (with plexiglass dividers and all precautions: masks, temperature, health questionnaire, sanitizer, etc.).

Some respondents said they expect things to return to normal, in terms of the tools and methods they use. Others say things will never be the same.

Totally scrapping in-person research. I’m not terribly sure in-person research will ever come back in the ways it previously existed. We haven’t used any virtual qualitative platforms just yet but I imagine we will in the coming months.

We had planned to do lots of in-person qualitative immersion work this year. That, and all other in-person qualitative has either been delayed until sometime in 2020 or moved online. As a result, we gave back a huge chunk of our budget.

Pre-COVID we conducted 15-20 in-person focus groups. Now in the current state of the world, I feel we may never go back to those traditional groups.

The key phrase there is “in the current state of the world.” Hopefully, once a vaccine is in place, even if we still have to wear masks more regularly, we will still conduct in-person qualitative – though of course, we don’t know what the impacts will be of mask-wearing on being able to read a focus group participant’s emotions! Several respondents offered variations on this take about in-person versus online research:

I hate not getting face time with consumers in real environments. Being able to stand with them and see how they interact with the environment in the store or look around the room to learn more about them and their personality when doing in-home interviews is sorely missed. Online qual can be good but it gives you tunnel vision to only what the consumer shows you. Lots of subtle cues are hidden.

Led to opportunities

For some, the COVID-driven changes have led to opportunities:

Marketing research has become even more strategic. We got invited to join a number of strategic initiatives since collecting VoC data via traditional ways – like clients directly talking to customers – is limited now.

Our use of virtual focus groups (online) has increased – we very rarely used it in the past. And we’ve been given license to test advertising creative, something that our brand team has always pushed back strongly against in the past.

Our biggest change has more to do with how we are reporting out insights. We are trying to stay ahead of the curve and push information out to the right team members as soon as we receive. This is to help exec teams make decisions based on these insights. This has been a huge undertaking for us but we’ve seen great engagement with what we are sharing.

My part of the company relies on IDIs with clients. We suspended all client research from lockdown until the beginning of July but have resumed. The only noticeable change so far is how many clients who weren’t willing to do video calls now are totally comfortable with it.

Another oft-mentioned change was bringing more work in-house that used to be delegated to vendors, which has some staffs in danger of being overworked.

We have stopped outsourcing projects and brought them back in-house, which means a lot more work for my department for reduced pay. No relief in sight. Morale has tanked and we are not motivated to go above and beyond since we are not even thanked for our efforts.

Acknowledging the impact that the shift to in-house has had, there were also many expressions of empathy for vendors, who have been forced out of the equation.

We have lost some vendor partners who have gone out of business due to the pandemic. This has been so unfortunate and also caused us to scramble to try to find new vendors to complete projects we had in the pipeline.

We’ve had to delay (for a year) or cancel some projects that we were looking forward to, which not only creates uncertainty for us but can make our vendor relationships uncomfortable, as they are obviously hurting from this.

Best and worst

Next we asked twin questions to find out what have been the best and worst outcomes of COVID-19 on their jobs as insights pros. The best part about the worst part? The large number of “n/a” or “nothing really” responses. Seems that some have been able to avoid being negatively impacted by the pandemic (or maybe they’re just really positive people!). But this response summed up the feeling of many:

Uncertainty all around as an insights professional, employee, parent, husband and citizen of the United States. These are very trying times.

As you might expect from a group whose job it is to think and talk about people and why they do what they do, the majority of the “worst” outcomes revolved around isolation, loneliness and a lack of connection to their colleagues and customers.

I’d say not being able to conduct in-person focus groups.

No water cooler chats with other people to trade insights and updates.

The “drive by” conversations don’t happen. This can be good and bad.

Loneliness, if you can call it that, of not seeing my fellow insights professionals and my energetic internal customers. No commute to ponder problem-solving. The distractions and challenges awaiting as soon as the workday has ended resulting from COVID-19 sometimes cannot be compartmentalized or go without addressing.

And, many mentions of the difficulties of working from home and having to navigate the needs of one’s four-legged and underage office mates.

We have two young kids (5 and 7) and it’s hard to work a full day and also be their teacher and entertain them during the day.

Also, the personal aspects of being a manager during an economic crisis.

Personally, I took a minor pay cut. Professionally, I had to furlough my entire team, which was incredibly difficult.

Verge of collapse

Many spoke of being asked to do more work with less budget and fewer staff. This, coupled with the often whipsaw nature of the research requests coming in (Focus on COVID and how it’s affecting our consumers! Forget COVID! Tell us where we need to go from here!), has left respondents feeling on the verge of collapse.

Burnout risk – the intense sense of mission and urgency of collecting up-to-date data for our teams risks burning out my team, and the change in working conditions and lack of in-person connection makes it really hard for me to ensure everyone is doing ok and to provide the emotional support resources we would normally rely on.

Additional workload for reduced pay and no gratitude expressed, just more demands. I am burnt to a crisp.

Brutal, soul-crushing hours. Everyone else is bored at home and I’m working nights, weekends, non-stop to keep up with the research demands.

More essential than ever

So, what about the best outcomes? Many were mirror expressions of some of the worst aspects, lighter yangs to the dark yins. The pandemic has forced companies to focus on the importance of insights, several said, leaving them busier than ever but also feeling more essential than ever. Many extolled the benefits of being able to work from home full-time. Rather than missing commutes, they were happy to not have them and relished saving money on transportation and/or parking and eating workday meals out.

More broadly, those respondents who are also department managers were excited at the prospect of being able to draw from a geographically wider pool of job candidates, now that being physically located near corporate offices is no longer a must for potential applicants. Others reported pride in how their teams have shown their mettle during the crisis, responding to the increased workloads and demands for insight with aplomb.

A HUGE appetite for insights from executive leadership, whether voice of customer, market impacts or competitor movements.

The ways we are finding to innovate have been amazing. Sometimes “shaking things up” is a great way to learn, improve and advance our work.

Our consumer research results have been elevated in importance to the highest levels of the organization.

My internal clients (stakeholders) have started to understand power of different methodologies (online discussion board, online IDIs, etc.).

We are delivering results that are used in Congress to make national-level decisions.

The potential to emerge in a different form through all this change.

Adapting to the new reality. Our company is spread out across the country and in some ways, we have had MORE contact with people in other locations, which has led to interesting new insights projects.

Many traditional methods of collection are off the table at this point, so we have had to be nimble and try new things. There has been an opportunity to innovate and use new technology that we probably wouldn’t have previously. Knowing that everything is in flux, we have had to become comfortable with being nimble and coloring outside the lines when needed.

Several respondents reported a renewed interest from internal audiences/groups in turning to the insights function to help the organization get a handle on the pandemic and its impact on the world.

Suddenly everyone relies on insights even more – and we became the go-to source of understanding what is happening to our business. This was always true but many didn’t realize it and paid more attention to sales than consumer behavior holistically. Now they really understand that other behaviors are more forward-looking indicators of what will happen to sales.

There were also multiple mentions of other unexpected side benefits to the pandemic in answers to the various open-ends, including higher response rates (especially among B2B respondents, who perhaps have more time on their hands or are stuck in their home offices) or improved uptake and effectiveness of certain digital tools, especially those involving video – likely as an offshoot of all of us being forced to live on Zoom calls to see our co-workers and family members.

Before COVID, getting traction on behavior change around research tech tools was slow. Now there is wide acceptance and fast adoption – because we don’t have a choice. Like most things in nature, in order to change direction, we must hit a wall first!

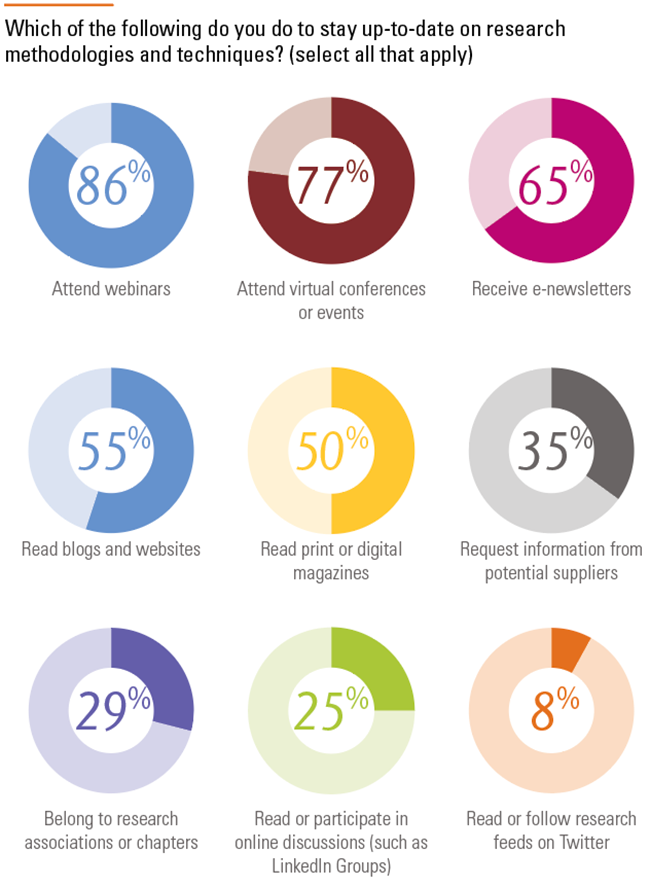

While many readers said they were busier than ever, several respondents reported having more time for professional growth during the pandemic, whether it was in the form of learning about their company and its industry or exploring new research-related topics or techniques. We asked respondents how they stayed current at a time when in-person events aren’t possible. Attending webinars was the most popular way to stay up-to-date on research methods, followed by attending virtual conferences or events, reading e-newsletters, blogs/websites and print or digital magazines.

While many readers said they were busier than ever, several respondents reported having more time for professional growth during the pandemic, whether it was in the form of learning about their company and its industry or exploring new research-related topics or techniques. We asked respondents how they stayed current at a time when in-person events aren’t possible. Attending webinars was the most popular way to stay up-to-date on research methods, followed by attending virtual conferences or events, reading e-newsletters, blogs/websites and print or digital magazines.

How do you feel about your profession?

While we gleaned many viewpoints on the topic from answers to other questions, we felt it was worth a more direct ask to find out how readers feel about their jobs as insights professionals. On a scale from extremely negative to extremely positive, “moderately positive” came in at 33%, with 18% extremely positive. Fifteen percent were smack in the middle, neither positive nor negative. Slightly negative clocked in at 10% and just 4 percent were moderately negative and 1 percent extremely negative.

The open-end responses to this question echoed many of those detailed above. Just as there were multiple expressions of optimism about the role and status of research, so too were there an equal number of gloomier takes. In the main, it seems to come down to how valued the insights function is by those in upper management. If an organization puts a real emphasis on listening to and hearing from customers, the insights function naturally has a chance to thrive. But if MR’s status is iffy to begin with, some respondents have said COVID-19 has been a convenient excuse to slash budgets and headcounts. As always, researchers seem aware of and realistic about how the business world works.

There are many things that excite me about the profession but I worry that we are perceived as, or hold on too strongly, to traditional approaches. In order to remain relevant, we need to adapt (or die).

With budgets being cut, it makes it harder to do quality research that will lead to a ROI. I worry that there is also too much demand and not enough of me (I am solo), which tends to never end well.

Truly remarkable

Taken as a whole, given the unprecedented nature of the times we are living in, the prevailing feeling of hope that our readers expressed throughout their responses to our survey is truly remarkable. They acknowledge their good fortune – they have jobs at a time when so many do not – while also realizing the weight of the responsibility being placed on their shoulders. But perhaps the most laudable thing is, they, for the most part, seem to welcome the challenge and are prepared to help their organizations make a path forward.

I believe this will be the defining moment of my career and feel incredibly proud of my team of researchers for the work they are doing. We are rising to this unprecedented occasion and doing intensive, impactful work to amplify the voices of people living through an incredibly hard time. Every day I see my company use our insights to better inform and support people around the world who are struggling through the pandemic. There’s never been a time I was more thankful for my training and experience.

The 2020 Q Report work life study of corporate researchers is based on data gathered from an invite-only online survey sent to pre-qualified marketing research end-client subscribers of Quirk’s. The survey was fielded from July 29 to August 12, 2020. In total we received 463 usable qualified responses. An interval (margin of error) of 4.5 at the 95 percent confidence level was achieved. (Not all respondents answered all questions.) We want to thank all of our client-side readers who took the time to complete the survey and provide their candid thoughts.