Cultivating growth

Editor's note: Kate Good is associate director of communications for the Plant Based Food Association and Institute. She can be reached at kate@plantbasedfoods.org. Catherine Cowan is insights lead on natural and organic brands and plant-based initiatives at 84.51°. She can be reached at catherine.cowan@8451.com.

The plant-based foods industry has experienced exponential growth in the past five years as consumers find more and more innovative options on grocery store shelves. The Plant Based Foods Association (PBFA) has been at the forefront of measuring plant-based food industry performance and working to better inform plant-based food companies, retailers and the broader food industry about key trends to further advance this burgeoning industry’s growth. While retail sales of plant-based foods are well documented, Julie Emmett, PBFA’s vice president of marketplace development, recognized a gap in research into the plant-based food shopper – more specifically, data that not only looked at spending habits across plant-based categories over time but also captured consumer sentiment and purchase intent to better understand the “why” and predict future trends.

Through strategic partnerships with top retailers, Emmett works to develop research that helps industry players understand the consumers driving the growth. This valuable information allows retailers to be at the cutting edge of merchandising strategies that make it easier for plant-based shoppers to find the products they're looking for and explore the ever-expanding variety and assortment of offerings that align with their personal values and lifestyle choices. In order to effectively implement strategies that meet consumer needs, core questions around how plant-based shoppers behave in the store and whether shoppers that engage with plant-based segments are actively displacing their animal-based purchasing need to be answered.

To provide the industry with insights into these questions, Emmett engaged 84.51°, the retail data, analytics and insights arm of grocery giant Kroger, to develop first-of-its-kind research that could serve as the foundation for consumer insights. PBFA and Kroger have a long history of collaboration and have produced industry-leading research on plant-based meat merchandising strategies that have influenced retailers across the U.S. The goal of this new research was to understand plant-based category engagement among Kroger shoppers. This includes the history of purchasing plant-based foods and shifts between plant-based and animal-based foods in order to identify where customers are migrating their spend. Understanding the interaction within plant-based categories and capturing shopper progression was also a crucial part of this research as it could provide invaluable insights to inform the plant-based foods industry as a whole.

The research, conducted via PBFA’s sister non-profit organization, the Plant Based Foods Institute (PBFI), was aimed at understanding how shopper behavior may be shifting between plant-based and animal-based foods. It aimed to uncover consumer attitudes and sentiment, leveraging 84.51° data science and insights experience.

Part 1: migration analysis

Methodology

The comprehensive migration analysis tracked purchase behavior of nearly 8 million households over two years – Year 1 (2019 to 2020) and Year 2 (2020 to 2021) – across five plant-based categories and five animal-based categories: milk; fresh and refrigerated meat; frozen meals; cheese; yogurt.

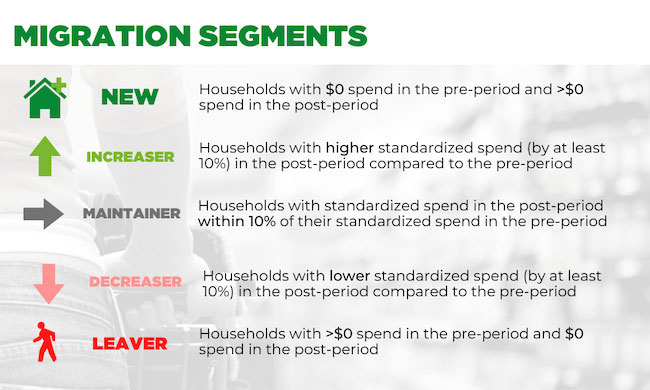

The 8 million households were categorized into five segments, ranging from shoppers new to the plant-based category to shoppers leaving the category (Figure 1). These segments are: New, Increaser, Maintainer, Decreaser and Leaver. Each household was classified from each target group into a migration segment by comparing spend in the post-period to the spend in the pre-period.

The 8 million households were categorized into five segments, ranging from shoppers new to the plant-based category to shoppers leaving the category (Figure 1). These segments are: New, Increaser, Maintainer, Decreaser and Leaver. Each household was classified from each target group into a migration segment by comparing spend in the post-period to the spend in the pre-period.

The questions at the center of the migration analysis included:

- To what degree are plant-based shoppers shifting their spend across animal-based products and plant-based products?

- Are there certain product groups that have large proportions of new engagers?

- How many new shoppers are there in plant-based foods?

- Are certain category buyers contributing to leakage?

Findings

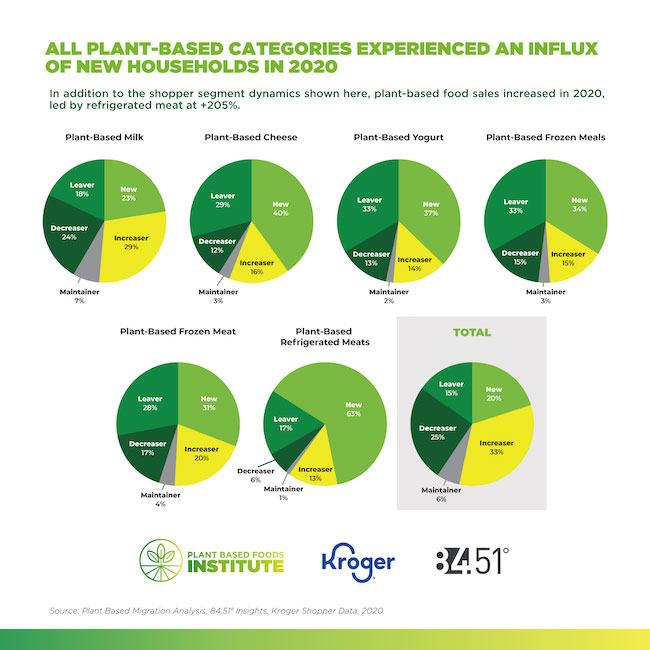

Year 1: In 2020, new households entered key plant-based categories.

During Year 1, the influence of COVID “pantry loading” was evident in consumer buying patterns. Households that were increasing or decreasing their spend in plant-based categories also increased their spend in animal-based categories.

In Year 1 (Figure 2), findings revealed new households trying different categories of plant-based foods. Plant-based meat had the largest portion of New households in 2020, with 63% of households classified as New. Plant-based cheese was the second highest with 40% of households classified as New.

In Year 1 (Figure 2), findings revealed new households trying different categories of plant-based foods. Plant-based meat had the largest portion of New households in 2020, with 63% of households classified as New. Plant-based cheese was the second highest with 40% of households classified as New.

Growth in plant-based New and Increaser households from 2019-2020 translated to sales growth across plant-based categories. Most categories witnessed double-digit percent growth, with plant-based refrigerated meat seeing increases of over 200%.

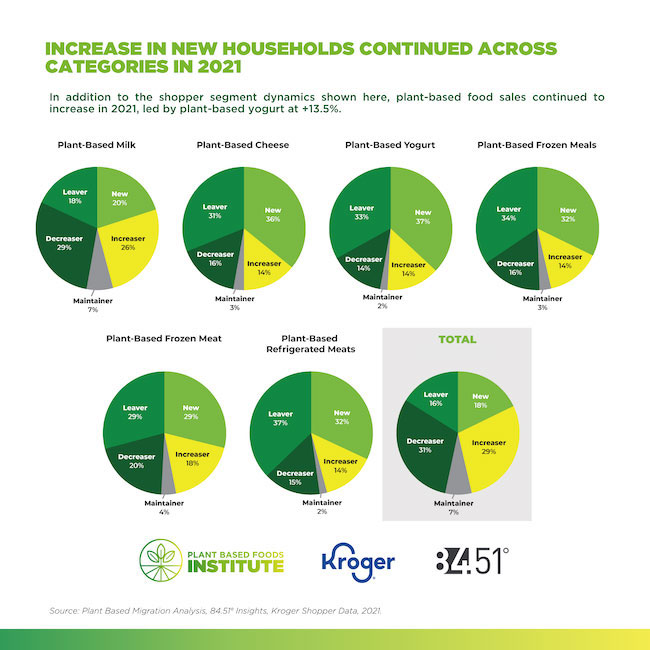

Year 2: In 2021, plant-based momentum grew with a steady flow of new households.

As the COVID purchasing noise began to slow down in 2021, a few key trends in plant-based category engagement emerged (Figure 3). Coming off a year with many new households across each plant-based category, New households continued to grow in 2021 and made up 18% of the migration segment across the total plant-based categories. This progression demonstrates that there is continued interest in plant-based categories building on the COVID bump from the year prior.

As the COVID purchasing noise began to slow down in 2021, a few key trends in plant-based category engagement emerged (Figure 3). Coming off a year with many new households across each plant-based category, New households continued to grow in 2021 and made up 18% of the migration segment across the total plant-based categories. This progression demonstrates that there is continued interest in plant-based categories building on the COVID bump from the year prior.

Following a year of record sales growth, a slowdown in category sales was expected; however, a majority of plant-based categories continued to grow. Most significantly, plant-based yogurt saw the largest sales increase of the plant-based categories with 13.5% growth; in addition, 37% of households were from the New segment. These numbers suggest there were successful new items and/or innovations in this space that brought new households in and notably, increased sales.

In both 2020 and 2021, Increasers of plant-based cheese spent the most on plant-based foods in total compared to all other product groups by $66.97 annually, with other categories seeing a change in spend ranging from $30-60 per year, suggesting that these households are the most loyal and engaged in plant-based overall out of all the target groups. According to 84.51°, once households are engaged with plant-based cheese, it can be assumed that this group will be more loyal to and engaged with plant-based foods overall.

Shifts in dollar spend

For plant-based households, animal-based engagement either decreased or remained nearly consistent from 2020-2021.

The average household that maintained its total plant-based spend decreased its total animal-based spend by $28.21 on average.

Among all households, plant-based sales increased 24.1% in 2020, followed by continued growth of 1.5% in 2021.

Part 2: plant-based foods shopper survey

In addition to the migration analysis, PBFI, Kroger and 84.51° conducted consumer research via surveys for households in the plant-based engager segment. The goal of this was to understand shopper attitudes and sentiments among the subsegments of plant-based Increaser and Decreaser households to better anticipate future trends for the plant-based category.

Methodology

The qualitative survey was executed online using the 84.51° consumer research real-time insights. A sample of 150 Kroger shoppers were selected based on known purchase behavior for each of two targets.

- Increaser segment (or households): The first target included behaviorally validated Kroger customers who were increasing their plant-based spend by more than 10% compared to the prior year.

- Decreaser segment (or households): The second target included behaviorally validated Kroger customers who were decreasing their plant-based spend by more than 10% versus the prior year.

Findings

The primary finding of the survey is that plant-based households are indeed purchasing plant-based foods instead animal-based foods and that 95% of the surveyed plant-based engager segment state that they are increasing or maintaining their plant-based consumption compared to the year prior, showing intent to continue engaging with plant-based foods. Among the group of plant-based Increasers:

- 43% report choosing plant-based milk instead of animal-based milk.

- Nearly 30% are choosing refrigerated plant-based meat and frozen meals instead of animal-based items in the same categories.

- Nearly 20% are choosing plant-based cheese and yogurt instead of animal-based products in the same categories.

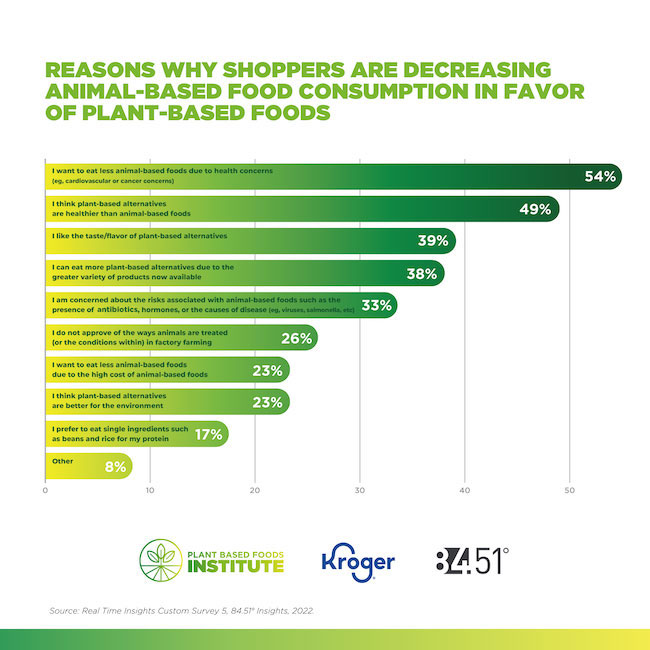

Surveyed plant-based Increaser households mention health as the leading reason why they are increasing their plant-based consumption (Figure 4), with 54% citing personal health concerns (such as cardiovascular or cancer concerns) and 49% stating they believe plant-based alternatives are healthier than animal-based foods. Note that these sentiments are reflective of surveyed plant-based consumer beliefs/motivations.

Surveyed plant-based Increaser households mention health as the leading reason why they are increasing their plant-based consumption (Figure 4), with 54% citing personal health concerns (such as cardiovascular or cancer concerns) and 49% stating they believe plant-based alternatives are healthier than animal-based foods. Note that these sentiments are reflective of surveyed plant-based consumer beliefs/motivations.

- Among plant-based Decreasers who were asked what would make them more likely to consume plant-based, 64% say lower pricing and/or more frequent sales and coupons and 58% say better taste and/or texture.

- For plant-based Increasers, when asked how shopping could be made easier, 61% cited price promotions and 29% said that recipes would be helpful.

While the category is very dynamic overall, the research provided a deeper understanding of shopper buying behavior by quantifying the actual shifts in spend by household for multiple plant-based and animal-based categories. At the same time, we now understand at a granular level what motivates shoppers across these 10 categories. There is no doubt there are shifts between animal and plant-based households and this migration analysis and consumer survey research delivered key insights into the multiple factors driving these shifts and illuminated the nuances of how various product categories behave differently.

Rapidly evolving

Conducting this comprehensive research across multiple categories over an extended period of time illustrates PBFA and Kroger’s commitment to understanding shopping patterns through the analysis of both plant-based and animal-based foods. Given the dynamic nature of the industry and how rapidly it is evolving, the question of how best to merchandise plant-based foods becomes more challenging, requiring research to help the entire industry understand best practices and assess strategies for action. This research (access the full report at https://pbfinstitute.org/migration/) serves as the benchmark study that will be conducted periodically to evaluate consumer interactions with plant-based foods as a whole and animal-based foods to better understand the shifts between them.