••• shopper insights

Splurging on mini moments

Stressed Europeans indulge in self-care

Despite continuing to be frugal with everyday purchases, European shoppers are splashing out on joy – turning to mood-boosting foods, stress-releasing toys and nourishing beauty products for comfort amid a backdrop of global conflicts, climate concerns and ongoing economic pressures that now shape daily life.

Circana’s Eat Play Love report finds that consumers across Europe are prioritizing purchases that give them more control over their lives and offer "mini moments of bliss." As European consumers become more selective about what they buy, they are channeling their money into luxury experiences, products and brands that deliver clear value, meaning or emotional return.

Bite-sized is the new normal as food is snackified: Snacks are no longer just eaten between meals but alongside – and instead of – a traditional breakfast, lunch or dinner. Thirteen percent of Europeans say they eat snacks instead of a main meal and 28% consume them alongside their main meal. Four out of 10 snack products consumed outside the home are now eaten at lunch or dinner. Nearly three-quarters of consumers snack while watching TV or browsing online, with almost half viewing it as a form of self-care. Spend on “snacking meals” is up 5% in food service outlets and up 10% in retail food service (a combined total of €64 billion).

Doggy bags are going mainstream with 20% of European consumers saying they now take leftovers home – citing saving money as the main motivation for requesting a doggy bag. The desire to reduce food waste also plays a role. Twenty percent of restaurant guests see taking leftovers home as an act of sustainability and a further 19% would like to see leftovers donated to charities. Twenty-six percent of consumers prefer environmentally friendly options and 27% are drawn to socially responsible brands.

There has also been a rise in secondhand toys and bargains. Parents are becoming more careful with what – and how much – they buy amid concern about the cost of living and the desire to be less consumerist. While toy sales are down, secondhand buying is on the rise. Fifty-one percent of European consumers say they’ve purchased “pre-loved” toys last year and the percentage keeps increasing. Many consumers are looking for a bargain when buying toys and online marketplaces like Temu and Shein are booming as a result. Thirty-two percent of European consumers say they bought a toy from a Chinese marketplace at least once during the second half of 2024. For 18-to-34-year-olds, the percentage increases to 58%.

Toys provide stress relief for big kids and little grown-ups. Play is now about emotional release and creative fulfilment, whether it’s intricate Lego Botanical sets, Jellycat plushies or Pokémon cards, consumers are spending on toys that bring out their inner child. Toys for ages 12+ now make up 31% of all European toy sales, worth €4.6 billion in sales – double their share from a decade ago.

In the age of “brain rot” and “zombie scrolling,” Europeans of all ages are rediscovering board games as an antidote to excessive screen use. Whether it's trading cards, jigsaw puzzles or spending the weekend in a board game cafe, consumers are turning to games for a much-needed opportunity to take a digital detox through play. Sales of card games were up 12% in 2024 and adult games increased by a staggering 22%.

As a confidence booster or a means of relaxation, smelling nice is essential to many consumers' sense of well-being. Sales of fragrances costing €150 or more were up 32% in 2024 to €653 million (compared to +8% growth for total fragrance). The lower end of the market is also doing well as budget-conscious shoppers look for more affordable alternatives as the sales of body sprays doubled in 2024.

This report draws from Circana's coverage of European food retail, food service, prestige beauty and toys covering sales of consumer goods in categories and SKUs across the U.K., France, Italy, Spain and Germany. Food retail covers six countries with additional data from the Netherlands.

••• brand research

Show me you love me

Gen Z want personalized videos from brands

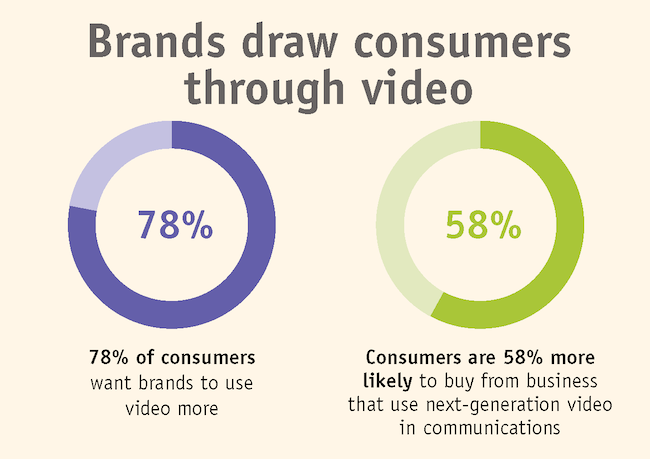

While 78% of consumers want brands to use video more, brands are falling short. The 2025 State of Video Technology report shows a very high demand for next-generation video, including videos that are personalized, interactive and AI-generated. The preference for next-gen video is strongest among younger, higher income and digital-first consumers.

Brands aren’t using video nearly enough in customer communications. Consumers are 58% more likely to buy from businesses that use next-generation video in their communications. Gen Z and Millennials are 20% more likely to see brands who use video as customer-focused and high earners are 13% more likely than low-income earners to feel the same. Nearly eight out of 10 consumers want more video and more than four out of 10 say they never get videos from brands they do business with, depicting a clear gap that brands need to fill to meet consumer expectations.

Personalized video drives loyalty. As in past years, personalized video is 4x more likely to make someone feel valued by a brand and 3.5x more likely to make them become or remain a customer. People punish brands when they don’t personalize. A sizable 44% of all consumers report that they get upset when communications are generic. This percentage jumps to 51% for Gen Z – 80% of whom also want communications to be more personalized in the future.

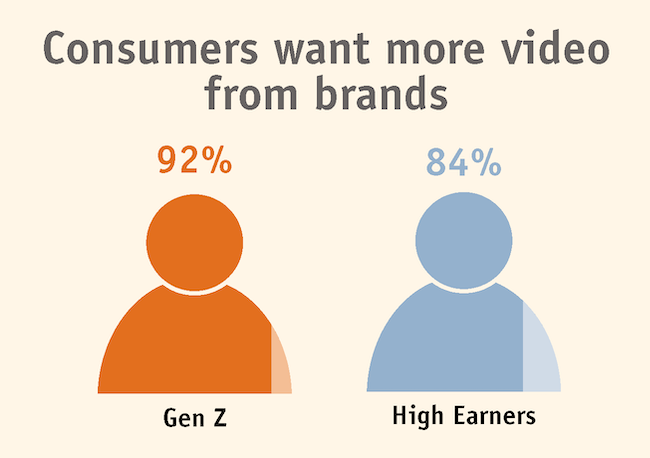

Consumers want AI videos from brands, especially when it makes things easy on them. They’re two times more likely to want an AI video generated from a document rather than the document itself. Younger consumers, high earners and those more comfortable with digital technology are the most interested in next-gen video. Gen Z leads the curve with a staggering 93% wanting personalized and interactive videos from brands. Right behind them are high earners (86%-88%) and digital-first consumers (85%-86%).

While consumers do want more video, the video quality is important. Nearly eight out of 10 feel more valued when a brand invests in high-quality communications. This jumps to 88% for Gen Z, 86% for high earners, 85% for Millennials and 83% for digital-first consumers.

Idomoo commissioned Atomik Research to conduct an online survey of 2,005 consumers in the U.S. and the U.K. from January 20-February 5, 2025.

••• health care research

Americans trust doctors, not AI

Generations unsure of health data collection

While 69% of Americans are comfortable sharing their health data to improve their own care, only 40% are comfortable sharing that same data with tech companies for AI-driven products. Despite growing AI integration in health care, data integration company Qlik found that only 28% would accept a prescription written solely by AI, highlighting deep-rooted trust concerns.

When asked to choose, more than twice as many Americans would rather donate blood (52%) than donate their health data (24%). This stark gap highlights just how deeply concerns about privacy and control shape attitudes toward health care innovation – even as AI continues to advance.

People love data for their own care but hate it for corporate AI. Comfort sharing data drops nearly 30 points – from 69% for personal care to only 40% for commercial AI. This sharp divide highlights public concern around privacy and profit motives, with one-third explicitly uncomfortable with commercial data use.

Trust goes to doctors, not AI alone. While nearly 71% reject medicine prescribed exclusively by AI, acceptance climbs to 63% when human clinicians oversee the process, emphasizing the essential role of human judgment in driving public acceptance of health care technology.

Gen Z trusts the government with health data yet seniors are skeptical. Over half of Gen Z adults (50%) are comfortable with the government using their health data for policy, while only 36% of seniors agree, revealing stark generational differences about trust and oversight in digital health care.

Most believe insurers use their data but doubt AI’s value. Though 41% think insurers already leverage their data, only 34% see current AI-driven care improvements, pointing to a disconnect that could slow down broader acceptance of health-focused AI initiatives.

With nearly 60% of Americans saying they’d share health data if compensated, it’s clear that trust and value must go hand-in-hand. Real progress demands more than promises – it requires new models that respect individual control and offer tangible benefits. The health care industry has a rare opportunity: reward patients for their participation, build true transparency and ensure AI drives outcomes that people believe in.

The Qlik AI in Healthcare Survey was conducted by Censuswide Research among 2,002 employed U.S. respondents 18+ between April 17-23, 2025.

••• shopper insights

Selectively spending

Financial pressure leads to budget reevaluations

Sustained inflation, supply chain challenges and global tariffs are influencing grocery spending and broader consumer behavior across generations and regions. Blue Yonder found that 85% of overall respondents are concerned about inflation’s impact on grocery prices, illustrating consumer unease and clear changes in purchasing decisions across the world.

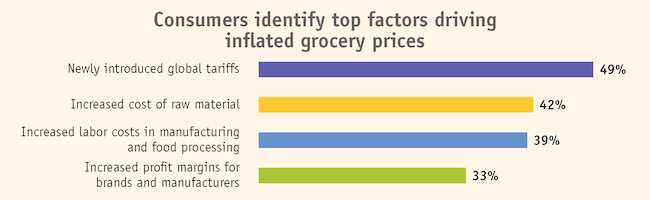

Nearly half (49%) of all respondents believe newly introduced global tariffs are the leading factor behind inflated grocery prices, followed by increased costs for raw materials (42%), increased labor costs in manufacturing and food processing (39%) and increased profit margins for brands and manufacturers (33%).

The perceived top factor driving inflated grocery prices differs across regions. Consumers in the U.S. (65%), the U.K. (56%) and the Middle East (50%) feel global tariffs are the leading cause of rising prices. Consumers in New Zealand (50%) feel that increased profit margins for brands and manufacturers is the top factor for inflated prices, while consumers in France (48%) and Germany (47%) believe the increased cost of raw materials is the leading cause of grocery inflation.

There is also a generational divide. Baby Boomers uniquely believe that increased labor costs in manufacturing and food processing are the leading cause for grocery inflation (52%), whereas all other generational groups believe global tariffs are the top cause of inflated prices.

Inflation’s grip on grocery bills is triggering global concern from consumers. Almost two-thirds of consumers (65%) report they would buy fewer grocery items across categories to cope with price increases, while 42% would shop at discount and wholesale stores. In addition, approximately one-third would prefer shopping based on promotions and discounts (36%) and switching to private-label brands (34%). Alcohol is facing the biggest budget cuts compared to other grocery categories, with one-third (33%) of consumers saying they would reduce alcohol purchases in response to inflation price increases.

To offset high grocery costs, many consumers noted they would be willing to cut back on discretionary spending. More than half (56%) of respondents are willing to cut back on clothing and footwear; this was also the top response by generations and regionally. Other top categories consumers are willing to cut back on include consumer electronics (46%), streaming/gaming subscriptions (43%), personal care and beauty (36%), appliances (33%) and automotive purchases (28%). Only 7% of respondents were not willing to reduce their other retail spending to offset grocery costs. Generationally, Baby Boomers are most likely to scale back on clothing and footwear (63%), compared to Gen X (59%), Gen Z (53%) and Millennials (50%).

Globally, consumers in New Zealand are the most likely to reduce spending on clothing and footwear (67%), followed closely by the U.S. (62%), the U.K. (61%), France (49%), Germany (49%) and the Middle East (47%). The next top category varied by country, with New Zealand (60%) and U.K. (54%) consumers most likely to reduce spending on streaming and gaming subscriptions, followed by Germany (42%), the Middle East (40%) and France (39%) willing to reduce spending on consumer electronics. These two categories – subscriptions and consumer electronics – were tied for U.S. consumers (54%).

The Blue Yonder 2025 Global Consumer Sentiment on Grocery Inflation Survey was fielded by a third-party provider in May 2025 with over 6,000 consumers across Australia and New Zealand (ANZ), France, Germany, the Middle East, the U.K. and the U.S.

••• pet care research

Pets over people

How animals help decrease stress and screen time

If you would rather hug your pet than talk to your partner after a stressful day then you're not alone. A new global survey of over 30,000 pet owners, commissioned by pet care business Mars and mental health company Calm, found that most pet owners (58%) prefer to spend time with their pet when feeling stressed – more than those who would choose their partners (32%), family (23%) or even children or friends (both 18%). In fact, 83% of people surveyed believe their pet has positively impacted their mental well-being.

The global survey across 20 markets highlights the powerful ways our pets improve our mental health and well-being. From encouraging us to switch off in our day-to-day with breaks from screens, work and chores, to offering silent comfort when words feel too much, the findings paint a striking picture of how pets are helping millions of people around the world find peace in an always-on world.

Sometimes, it's not what pets do, it's just that they are there. More than half of pet owners (56%) say their pets provide company without the need to talk during stressful times. While others find chatting to their pet helpful – with nearly a quarter (23%) saying their pet provides a space for them to express worries or concerns without expecting a response. A huge 84% of pet owners say the simple presence of their pet is relaxing, offering a sense of calm that doesn't require words or actions.

The survey also reveals how our pets' behaviors give us daily nudges towards better well-being habits. They are reminders to step away from the daily grind. Almost eight in 10 (78%) say their pet reminds them to pause and take a break from work, chores or tasks, with 50% saying this happens daily – a gentle reminder to stop, breathe and reset. Pets calm the mind with 73% of owners say their pet encourages them to stop overthinking or worrying – helping them feel calmer and more centered.

Seventy-three percent of pet owners say their pet encourages them to spend time outside. Even screens take a backseat when pets are around. Seventy-seven percent say their pet encourages them to take a break away from screens – and for half (50%) it's a daily reminder to unplug, a vital counter to constant scrolling and digital burnout.

The research was conducted by YouGov Plc on behalf of Mars. The total sample size was 31,299 adults across 20 markets. Fieldwork was undertaken between February 19-March 31, 2025.

••• employee research

Good luck explaining that sudden tan

Workers take stealth vacations on the company dime

In a survey commissioned by ResumeBuilder.com, 41% of workers surveyed said they have engaged in “quiet vacationing” this year – that is, they have taken time off without officially requesting it, often continuing to work or maintaining the appearance of working while away. A further 39% planned to do so this summer.

Gen Z workers are the most likely to engage in the practice, with 66% saying they've taken time off without notifying their employer. Quiet vacationing is also more common among executives (65%) and fully in-person workers, all of whom reported taking a secret vacation in 2025. "Executives often have the flexibility to step away discreetly, while Gen Z workers are more likely to find creative ways to stay connected while traveling or taking time off," says the firm’s Chief Career Advisor Stacie Haller. "Many employees feel they don't receive enough vacation days and want to save them. In-office workers may also be quiet vacationing as a way to push back against the lack of remote or hybrid options."

Among those who quiet vacation, the primary reasons include saving PTO for another time (33%), fearing they might look less dedicated (14%) or not wanting to use PTO at all (13%). Others cite being paid out for unused PTO (12%), anxiety about asking (8%), having a request denied (8%) or concerns about layoffs if they take time off (7%).

The survey also found that 75% of quiet vacationers maintained the appearance of working a full day. Many answered e-mails (69%), responded to instant messages (60%), took calls (54%), attended virtual meetings (49%) or met deadlines (41%) while away. Some used tools to bypass monitoring software (32%), relied on AI to boost productivity (28%) or had coworkers cover for them (26%). Nearly two-thirds of workers who joined virtual meetings during a quiet vacation used a virtual background to hide their location.

Few workers faced serious consequences for quiet vacationing, though 37% say their employer found out. Of those, 30% were denied a promotion, 29% lost out on a key project, 27% were denied a raise and 16% were fired. More than half of quiet vacationers say they don't feel guilty about it.

This survey was commissioned by ResumeBuilder.com and conducted online by the polling platform Pollfish in July 2025. The survey included 1,200 full-time U.S. workers.