Editor’s note: Jon Christens is director of communications at media agency Kelly Scott Madison, Chicago. This article is an edited excerpt from Kelly Scott Madison’s fall 2016 issue of State of Media.

This is the second of a two-part article looking at the state of brick-and-mortar retail. In Part I we looked at what is driving in-store shopping, as well as a breakdown of what is used to drive customers into stores, focused on understanding the tactics that keep individuals coming back. Today we will look at how consumers are taking to new retail technology that is aimed at keeping them engaged as well as to optimize the in-store experience.

Tech-savvy retailers

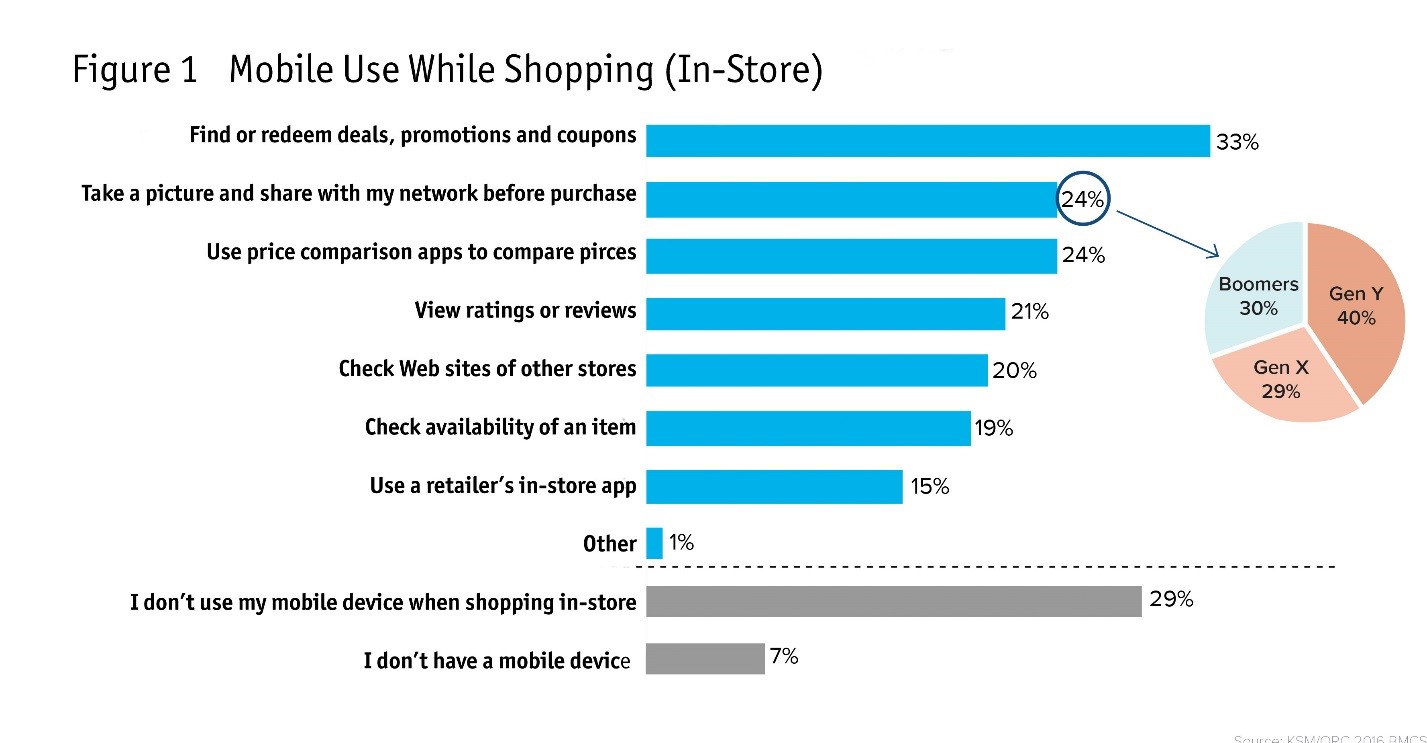

Overall, 2016 survey figures show that some consumers are still struggling to find usefulness in utilizing their mobile devices while shopping in stores. Even though 33 percent indicated they plan to use their mobile device while visiting a store to find or redeem promotions or coupons (Figure 1), 29 percent stated they don’t plan to use their mobile device while shopping at all. These numbers represent somewhat of a backtrack from 2015 Holiday Shopping Study responses, when 44 percent claimed they would use their devices to find promotions or coupons and just 27 percent felt it wasn’t necessary for in-store shopping. While year-over-year fluctuations like this are expected, it seems that retailers haven’t made much progress lately in convincing certain shoppers to engage on second screens.

The question then becomes, who exactly are these individuals that don’t utilize mobile devices when shopping? Unsurprisingly, most are Baby Boomers, with 40 percent claiming this distinction. About 30 percent of Gen X respondents said the same, and just 13 percent of Millennials shunned phones while shopping in stores. So, what’s the good news for tech-savvy retailers? That leaves a majority of consumers, across all age groups, stating that they do utilize mobile devices in these circumstances. Of course the younger the consumer, the more likely this will be the case, but the lesson here is that shoppers from every generation are finding ways to connect while browsing in stores.

Besides searching for deals or coupons, what else are they doing on these devices? Tied for second place, 24 percent of respondents claim they are taking pictures to share potential purchases with their network prior to buying, while another 24 percent are using price-comparison apps. The popularity of seeking public approval by sharing photos on social prior to purchasing is certainly an interesting phenomenon. A 2015 survey conducted by fashion site Shopa found that “chelfies” or changing room selfies, were driving purchasing decisions for all genders. Men look for an average of four likes on a photo prior to committing, while women seek an average of three likes. KSM’s findings show that this activity isn’t just limited to younger audiences. Of those who say they do this, 40 percent are Millennials, 29 percent Gen Xers and 30 percent Baby Boomers.

Viewing ratings or reviews, checking other stores’ sites and looking up item availability came lower down in the activity rankings at 21, 20 and 19 percent, respectively. These were followed by using retailers’ in-store apps, which appeared lowest on the list at 15 percent. The bottom ranking for apps could be due to either low popularity from consumers or simply a lack of brand apps in existence. Regardless, it doesn’t bode well for the concept of custom app development for retailers, and reinforces the idea that optimizing a brand’s site to work well across all devices (especially mobile) is a more cost-effective strategy in the long run.

Push notifications

Push notifications have also received a lot of buzz over the past few years, and for good reason. Anytime a retailer can establish a direct and uninterrupted link with its customers, positive things usually happen. That said, only 21 percent of total respondents have ever received a mobile alert that subsequently caused them to enter a store. As to be expected, audience members who did claim to have taken this action skew younger, with 49 percent being Millennials, 29 percent Gen Xers and 22 percent Baby Boomers.

The content of those alerts most often focused on coupons or ongoing sales, with 47 percent and 39 percent marking these two options, respectively. Ultimately, push notifications targeting in-store shoppers still have much ground to make up in terms of proving to be effective. Evidence of this can be seen when revisiting the breakout of marketing elements that consumers claim are most likely to drive them into stores, where just 14 percent of total respondents feel mobile alerts or push notifications are either extremely or very influential. As technology and devices continue to evolve these sentiments are bound to grow, but for the time being retailers would be better served following the same advice as given for apps: test any of this activity through third-party providers rather than spending money and resources to build custom interfaces.

Privacy issues

New technologies currently in place and ones coming down the line to help physical retailers maximize customer data collection and efficiencies are also exciting aspects to ponder. Though as is the case with many new developments, it seems that privacy issues are leaving some with conflicting feelings about in-store behavior monitoring. Of total audience responses, 31 percent claim they don’t like it at all, while 37 percent say it’s not a bother if it benefits the customer. That left 13 percent saying they outright like the idea of behavioral tracking, and 20 percent unfamiliar with this technology. Similar to online behavioral advertising (via AdChoices), it appears that an education campaign needs to be launched in order to boost positive feelings and understanding about the beneficial ways that retailers plan to use in-store tracking data. It remains to be seen who would pick up that torch, but the National Retail Federation is certainly a likely candidate.

Low on the priority list

When looking at the emerging in-store technologies that shoppers find exciting, the themes of convenience and time-savings continue to present themselves. Touch-screen kiosks are listed as the most intriguing, with nearly 40 percent of respondents ranking it highly on an interval scale. Next came near-field communication shopping with 32 percent ranking it high, which is interesting given its relatively technical nature, and rounding out the top three high rankers is mobile pay at 30 percent. Virtual or augmented reality experiences and smart dressing rooms fell in the middle of rankings, while advanced display, personalization and tracking technologies (e.g., holograms, 3-D printing and beacon tracking) came last.

In the end, overall enthusiasm with new in-store technologies isn’t particularly high for the average U.S. consumer. This could be due to underexposure, since these type of executions are often only installed and valuable at flagship stores, or it could be due to general disinterest.

Time and again, data has proven that unless something is increasing value or saving time, it doesn’t rank high on the priority list for most consumers. Retail marketers should certainly take note of this, and ensure that their marketing efforts are finding the right balance in order to drive robust store traffic well into the future.

Methodology: This report presents the findings of a survey conducted among a demographically representative U.S. sample of 1,011 adults, comprising 503 men and 508 women. Completed interviews are weighted by five variables – age, sex, geographic region, race and education – to ensure reliable and accurate representation of the total U.S. population 18 years of age and older.