Editor’s note: Uroš Berisavljević is head of insights at market research firm EyeSee. This is an edited version of a post that originally appeared under the title, “Market research, industry re-inventing itself.”

Who coined the ubiquitous business term market share in the 1930s? Nielsen. Do you know who ordered the first commercial computer in the 1950s that was used for civilian, non-governmental purposes? Nielsen. Nielsen, a leader in the business of market research, was at the forefront of the informational revolution. However, the exciting innovation-driven beginnings do not reflect the current state of the marketing research industry.

Who coined the ubiquitous business term market share in the 1930s? Nielsen. Do you know who ordered the first commercial computer in the 1950s that was used for civilian, non-governmental purposes? Nielsen. Nielsen, a leader in the business of market research, was at the forefront of the informational revolution. However, the exciting innovation-driven beginnings do not reflect the current state of the marketing research industry.

Van Westendorp’s sensitivity meter was introduced in 1976 and, with occasional brush-up, it is still widely used today as if nothing has changed.

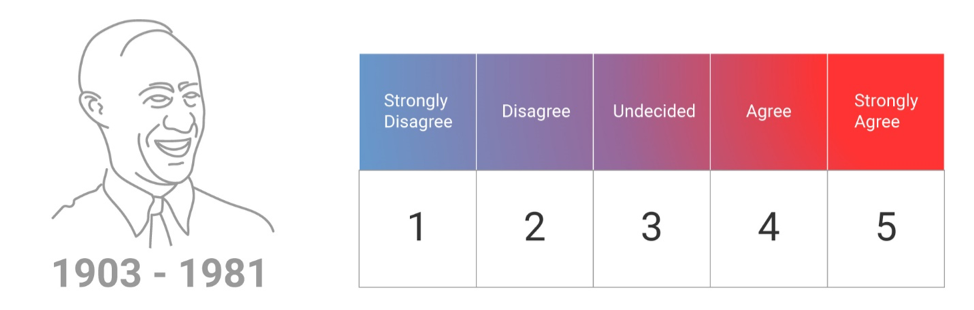

Likewise, Rensis Likert invented the Likert scale, the most consistently employed research tool with minor fluctuations in the debate surrounding its misuse. Likert passed away in 1981 – before the majority of my colleagues were even born.

This scale presented a true breakthrough when it was introduced in the 1930s. What is the future of an industry that uses tools from almost a century ago?

Understanding innovation

As Noah Brier, co-founder of Percolate noted, the word innovation has come to represent so much today that it almost lost its potency and meaning.

To understand it as a phenomenon and grasp its manifestations in our industry we need to look back at the past. Usually, when trying to pin down the nature of innovation, most assume a linear progression – one small idea on top of another one. The reality takes a different form.

“Innovation is taking two things that already exist and putting them together in a new way.” – Tom Freston

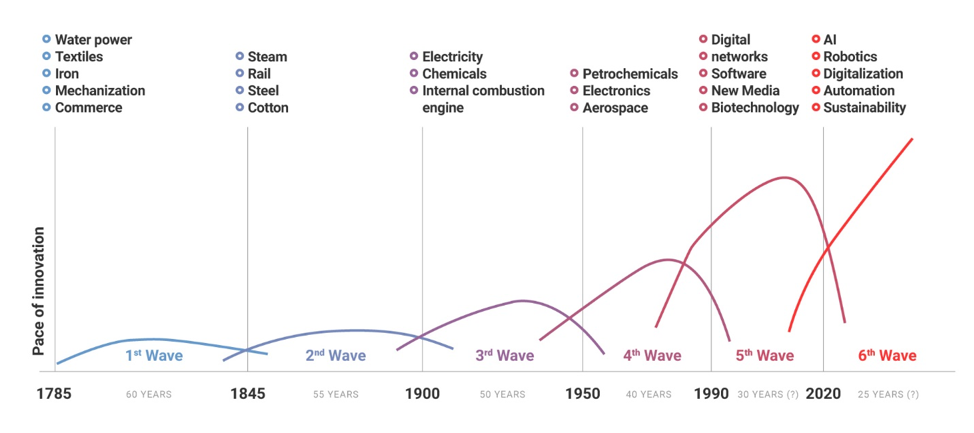

Using historical data on technological advances, economic structure, salaries and political unrest, theorists Chris Freeman and Francisco Louçã postulated the so-called “Kondratiev waves” to describe clear patterns linking innovation to the performance of the economy. The breakthroughs we distinguish as innovative are a consequence of accumulative knowledge and evolution rather than revolution. Take for instance technological waves of innovation: at each stage, one technology is pivotal and defines the who global economy. We see the trends growing and then steadily declining.

Right now, we are entering the sixth wave of technological innovation and the shift can be also observed through eminent changes in the market research industry. We increasingly move away from the survey to automation, providing behavioral insights and big data interpretation. Consequently, old conglomerates such as Nielsen and Ipsos already face up to 5 percent drop in sales in comparison to the same semester last year, while GfK was bought off by KKR, effectively no longer in the market research business. Simply put, a conventional research and business strategy are no longer adding up.

The new high

While the state of the conventional market research is on a decline, new opportunities are emerging. The most notable factor is big data, which begins to dictate how we understand user and consumer behavior by the minute, but also shapes clients’ demands. Further, Satya Nadella, the CEO of Microsoft, predicted that the true commodity of tomorrow would be – human attention.

Trends such as big data will be here to describe and provide numbers. However, turning data into insights means going a step back to uncover the reasons behind (consumer) behavior in a predictive manner. I believe the path to growth is clear – behavioral research based on subconscious insights.