Inflation and shifting consumer behavior

Editor’s note: Teodora Cvetkovic is insights manager at EyeSee, New York.

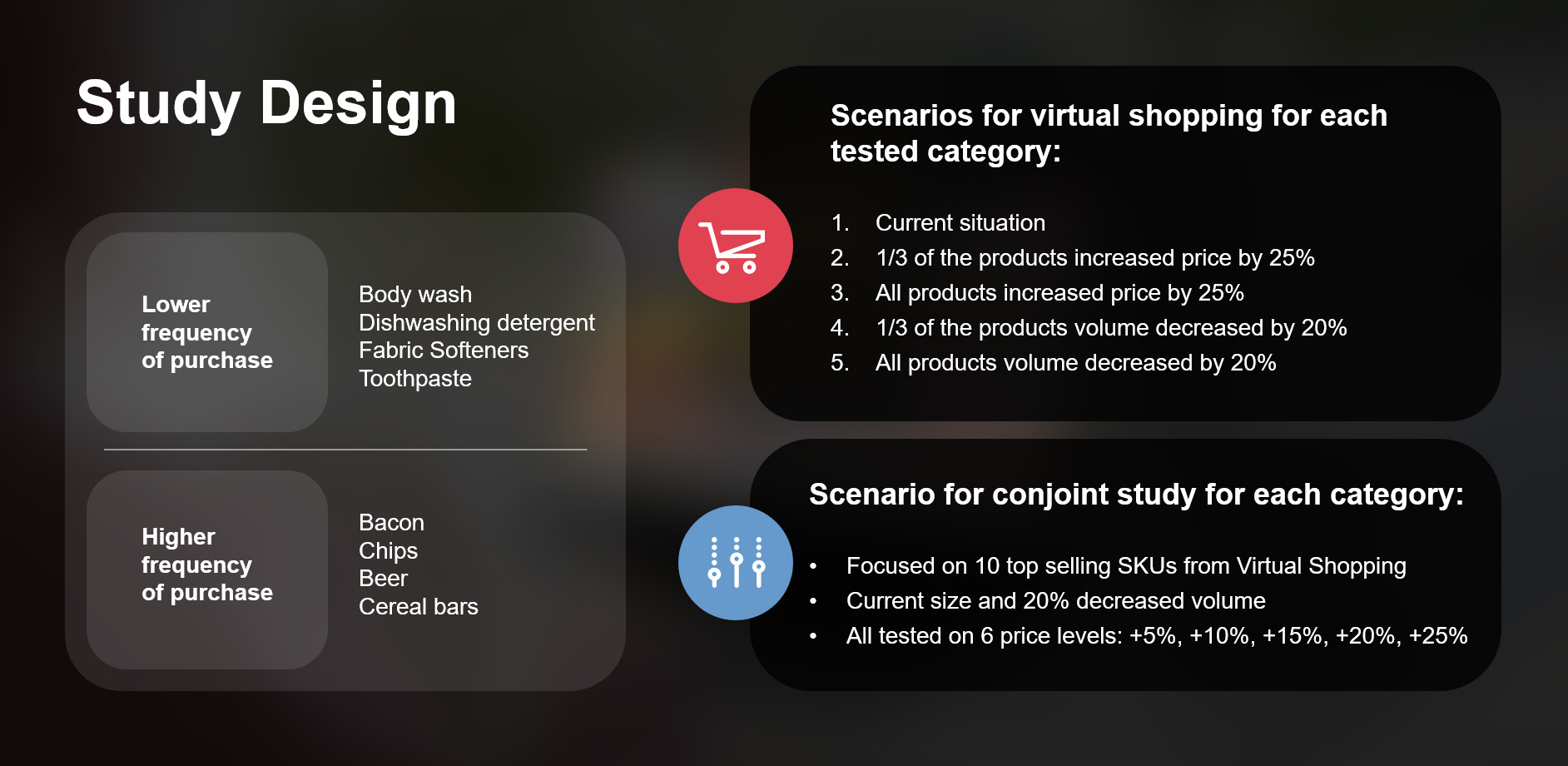

What are the best shopper strategies to cope with ongoing inflation for both CPG and retailers? To answer this, EyeSee conducted virtual shopping studies and conjoint analyses on the impact of pricing adjustment. The study collected more than 6,500 responses across six categories.

Both price increase and volume decrease were at a high end, 25% and 20%, respectively. Why? Essentially, the goal of the study was to understand which direction these scenarios would sway consumers. Using more conservative price and volume adjustments would give the same indication of direction, only with a less noticeable magnitude.

Are brands at the mercy of price anchoring?

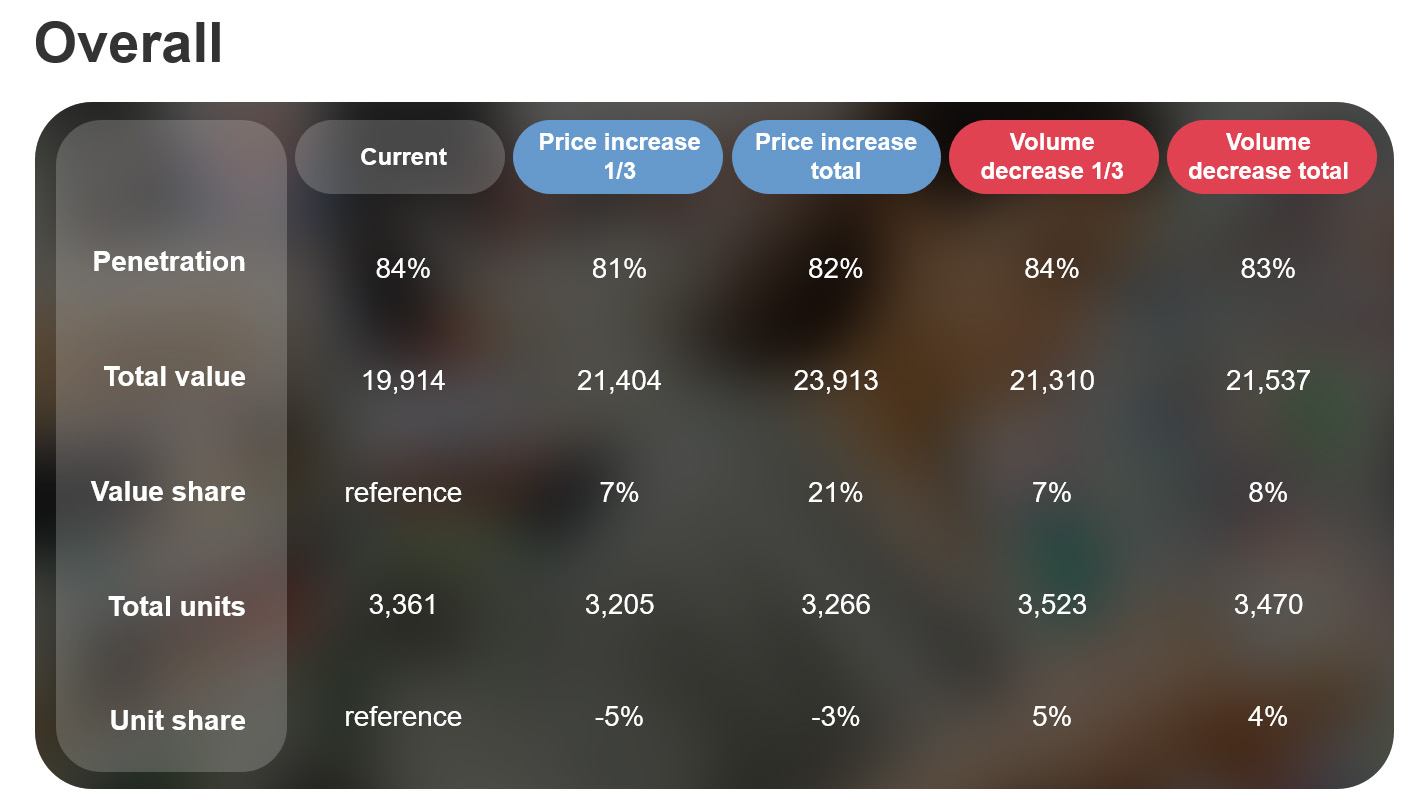

Overall, when looking at all categories combined, we've noted that strategies don't have a negative impact on category value growth. In the scenarios with the price increase, the value growth is between 7% and 21% due to an increase in price per product bought. However, the number of units bought per shopper drops. When the whole category boosts the prices, the total units only decrease by 3%.

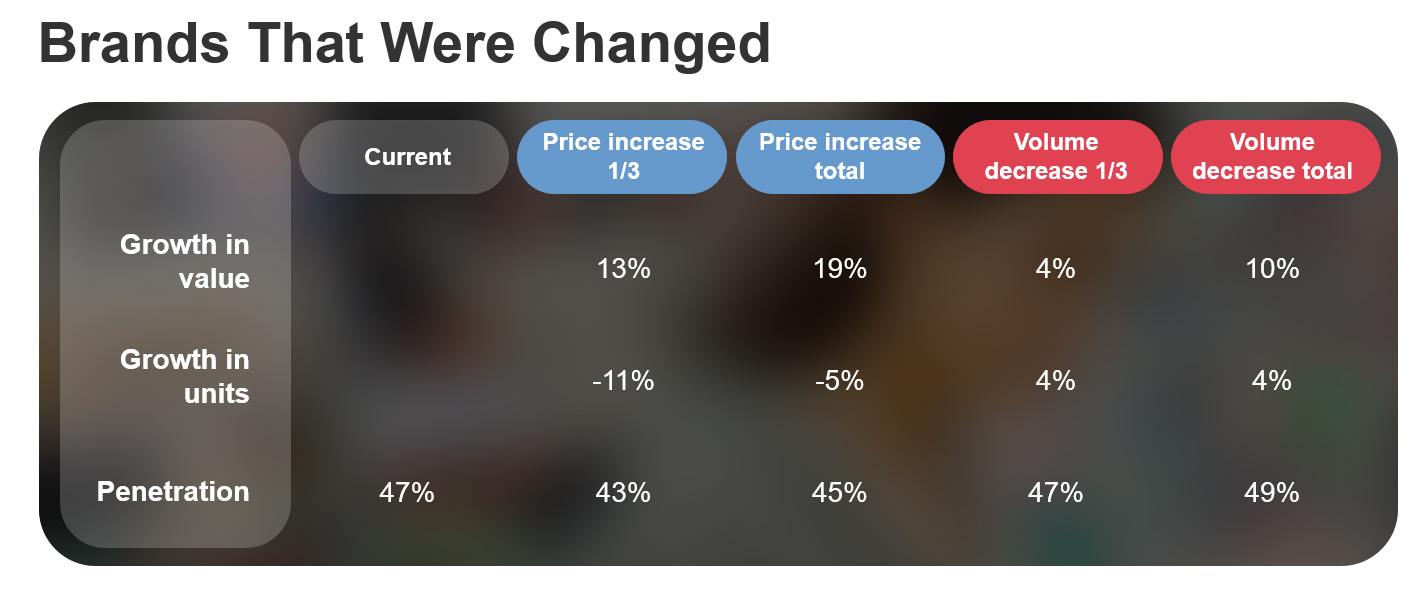

On the other hand, in the scenario that the leading brand was the only one to increase the price, units dropped by as much as 5%. This indicates that shoppers use context and search for prices as anchor points to inform their decision. Also, the category grows about 7% when the volume decreases, but the price stays the same. In these scenarios, shoppers buy 3%-5% more units.

So, if just some brands increase their costs and it is possible for shoppers to compare the price tags on the shelf, the most price-sensitive consumers will walk away from the shelf. However, when the whole category increases the prices, comparison shopping makes the differences in pricing less obvious, so consumer behavior remains consistent. Interestingly, we also noted that the number of people willing to give up the purchase entirely in price increase scenarios doubled (from 6% to 12%) – and tended to not choose any private labels instead.

Expanding units or value?

No doubt, the best case for the CPG companies and retailer is a total category price increase. In the scenario with a 25% price increase for all, the sales growth in value is 19%, while only 5% fewer units are sold.

It is completely plausible that you are unsure about competitive action and what shelf price context will look like; one cannot always tell if the competition will opt to increase prices or decrease volume per unit. If that is the case, your pricing decision rests on a simple question: which KPI is more important to your brand and portfolio – unit share or value? The price increase will surely result in an increase in revenue but will have fewer units sold in total – even more so if you are the only brand to increase prices (e.g., category leader). In our extreme scenarios, you might lose up to 7% of your customer base, as our study showed that penetration decreases from 47% to 43%.

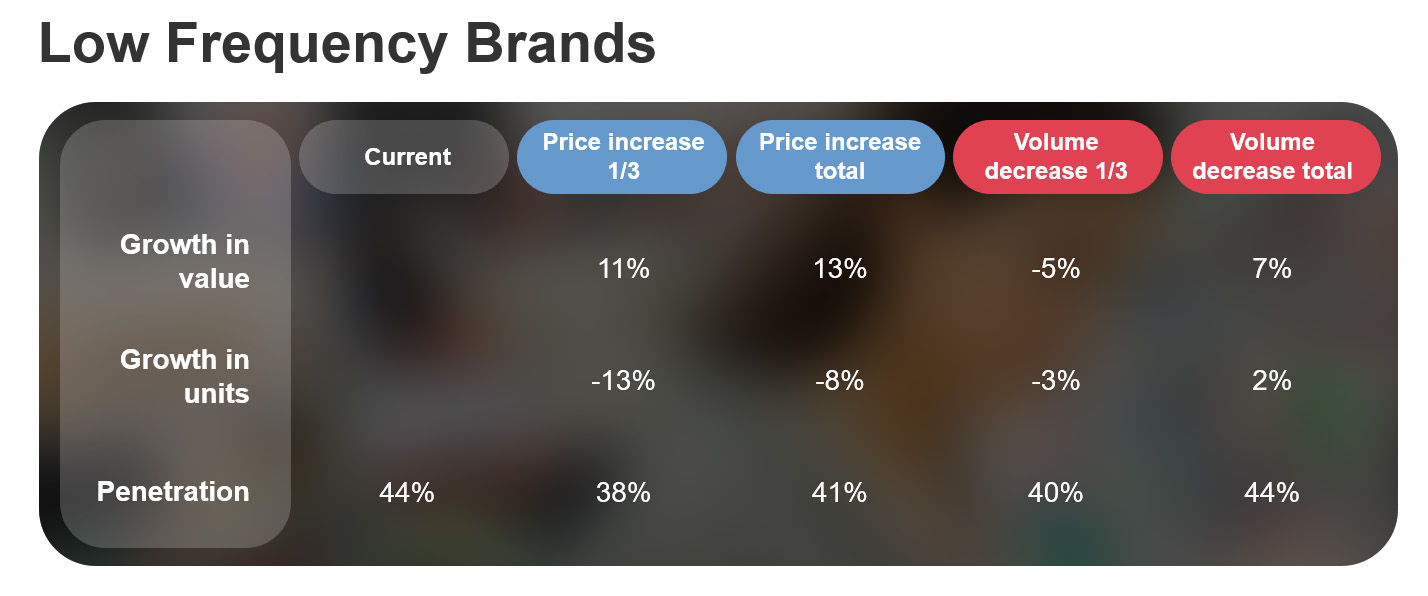

Low frequency categories are more vulnerable (for now)

Purchase decisions are category specific, and it is imperative to draw a clear line between high and low frequency items if you want to narrow down on a good pricing strategy.

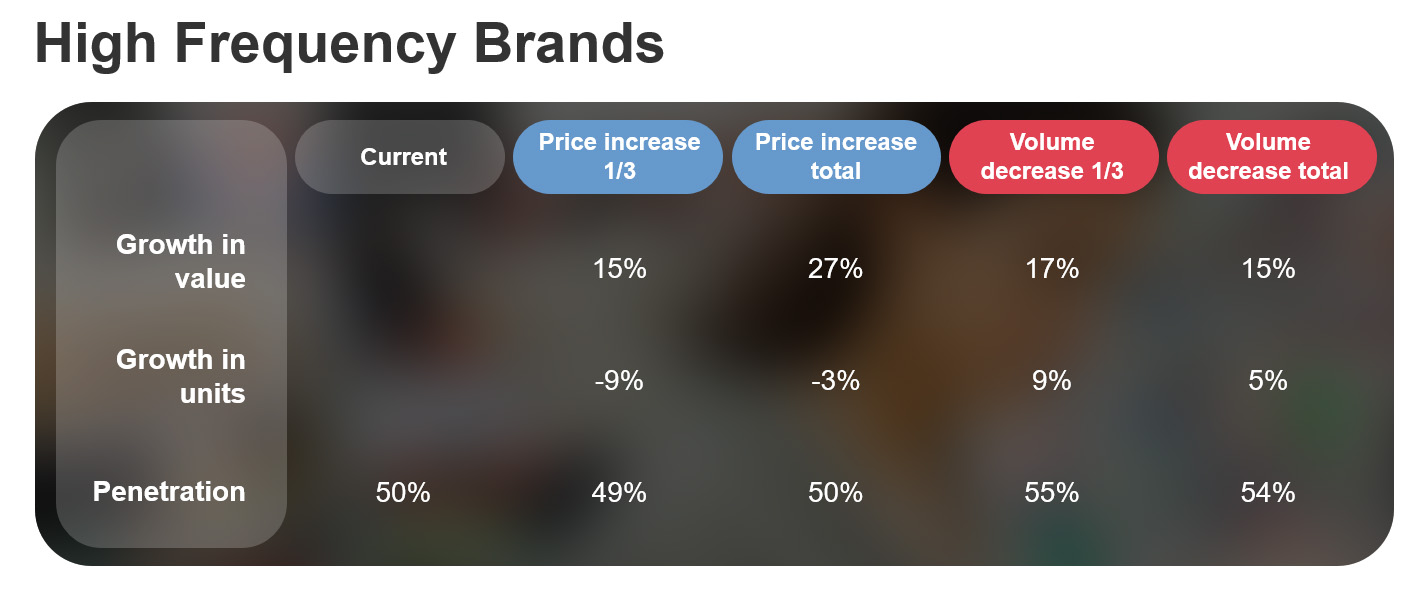

Our findings indicated that leading brands changing their prices and volume in low frequency categories are worse off than leaders in the high frequency segment. In low frequency items with a price increase, penetration dropped by as much as 6%. We've seen that shoppers might postpone their purchase altogether due to higher sensitivity to price fluctuation.

To make matters even trickier, volume changes will likely have an even more negative effect on penetration. When the leading brands are the only ones that decrease their quantity per unit, their sales and unit sales drop. In this case, shoppers might expect a lower price per quantity for large quantity SKUs.

Although considered essential, as mentioned, consumers can postpone purchases in the low frequency category and search for better deals elsewhere in case their favorite brands increase prices. A similar trend can be seen in the high frequency category, too – there is a general switch toward alternatives and exploration of different brands.

So, while it seems counterintuitive, now is the time to think about testing and widening your portfolio – from different pack sizes to entirely new products with added benefits – to not only intercept the delay in purchases or switching but to truly understand what your consumers need and how you can further support them.

Inflation, unpredictability and consumer behavior

To sum up the learnings so far:

- Shoppers seem most adaptive in the scenarios where the whole category raises prices;

- Volume decreases come with bigger risks than price increases, so in case you opt for it, make sure to be as transparent as possible;

- Low frequency brands might experience a bigger drop as (at least in this point of crisis) some shoppers opt out of purchase altogether, rather than switching to another product or brand

Previous periods have been riddled with crisis, unpredictability and shifting consumer behavior. The only way to stay on top is to regularly feel the pulse of your shoppers and understand how and why they behave the way they do at a given time. While it might be counterintuitive to traditional crisis management measures – do research and innovate today as it may very well be the difference between winners and losers of the inflation tomorrow.

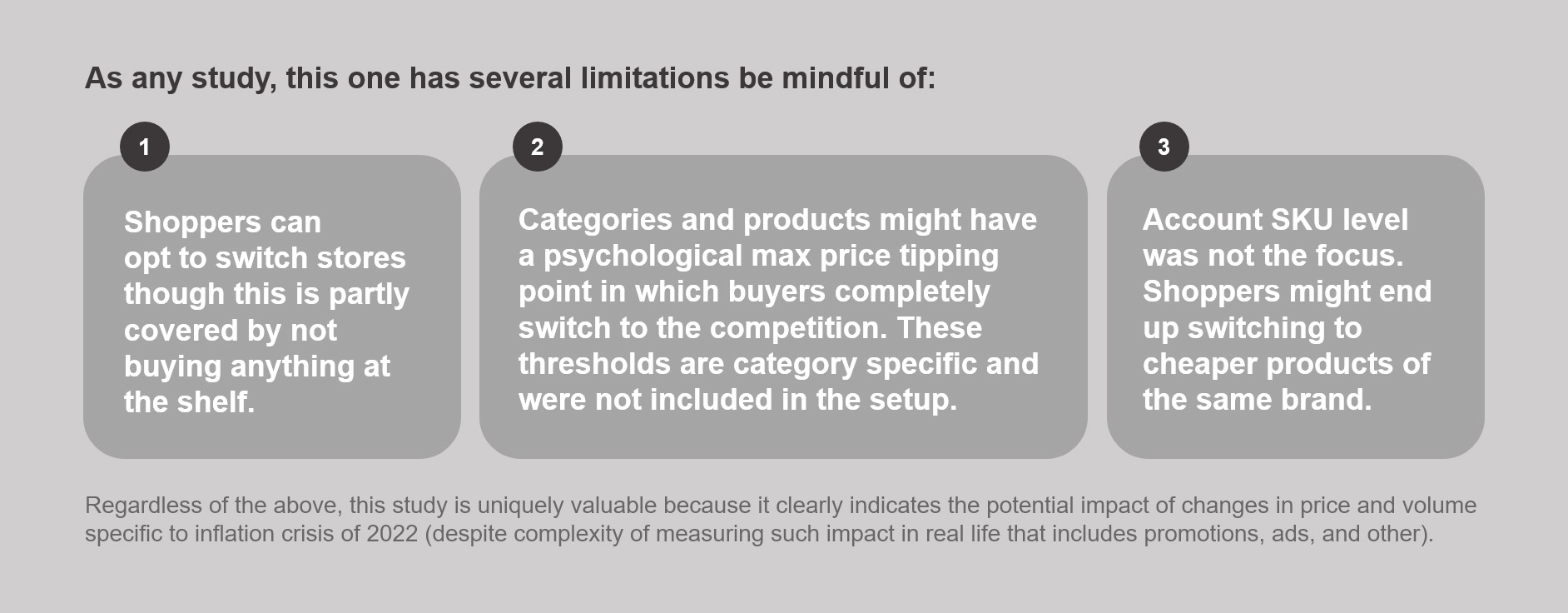

Methodology note

The methodology used in this study was a combination of behavioral and traditional methods. One group of respondents was exposed to virtual shelves where they could discover different products in a realistic virtual environment. After the virtual shopping exercise, respondents completed a survey that focused on their views on the current global situation and their behavior. Another group of respondents partook in a conjoint exercise that was followed by the same survey. Check out our previous conversations about pricing strategies with shopper experts from Kraft Heinz and Kellogg.