Editor’s note: Maria Mascaraque is health and wellness analyst at market research firm Euromonitor International, London. This is an edited version of a post that originally appeared here under the title, “What the new health and wellness data is telling us: A look into latest trends.”

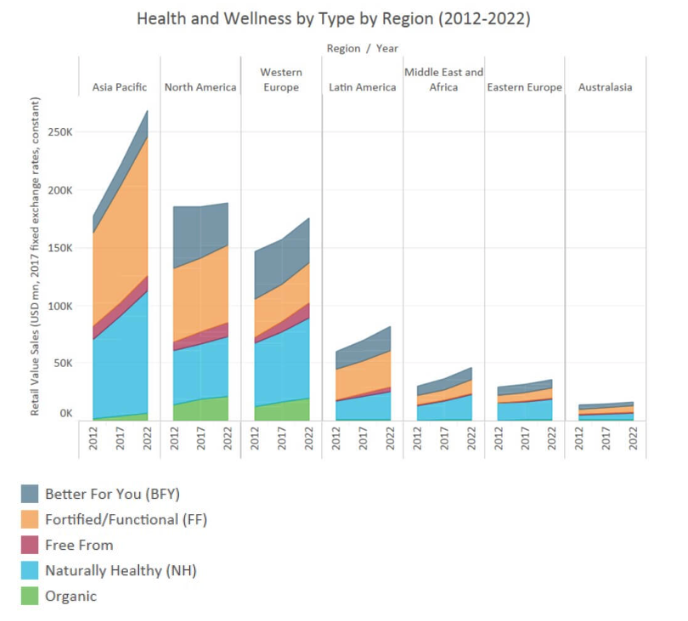

In 2017, health and wellness continued to look to Asia Pacific, the Middle East and Africa for global growth, with these two regions posting retail value growth of 3.3 percent and 4.2 percent, respectively. This is noticeable in the ranking of leading growth markets globally, headed by Egypt and India.

Conversely, North America saw an outright decline in health and wellness sales between 2016 and 2017, with categories such as reduced fat packaged food and reduced sugar soft drinks being predominantly responsible for this trend, both declining over 5 percent in 2017. The better for you offering (reduced fat, sugar, salt and caffeine) is considered heavily processed by consumers, due to its long ingredients list, and therefore is not doing well in most developed countries.

In fact, the world of health and wellness is moving toward products perceived as more natural and healthier which has resulted in growing demand for organic, free from and naturally healthy products globally over the last few years.

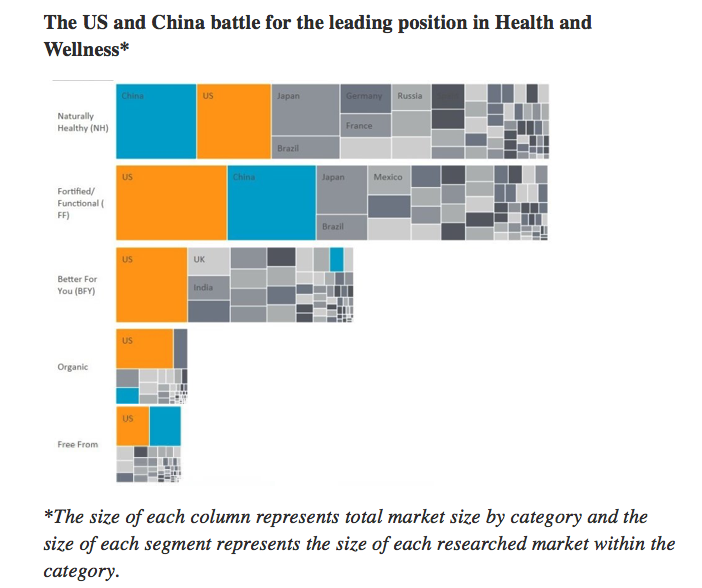

In terms of retail value growth, the organic offering leads growth figures in 2017, with China, unsurprisingly, driving this trend globally, with 19 percent growth. Organic milk formula and organic baby food lead the trend in the country as parents are looking for safety and confidence in products for their babies and are willing to pay a premium for them following past safety scandals in China in relation to milk formula.

The U.S. organic market, however, keeps leading in absolute growth terms, as the American consumer is looking for holistic approaches and is seeking organic ranges, simple ingredient lists, no artificial additives and non-GMO products. In fact, in clear recognition of where blossoming competition is occurring, mainstream brands took the organic plunge to maintain share in the U.S.

The free from offering (free from gluten, dairy, lactose, meat and allergens) stands out too. It is boosted by the health-conscious consumer that perceives this offering as more natural and healthier, mainly in developed countries, where the trend has gone beyond intolerance and allergies. Although free from dairy is the largest category, with China clearly leading the market, free from gluten showed the largest absolute growth over the review period (2012-2017), with the U.S., Italy and the U.K. being the largest contributors.

Although organic and free from are the categories with the strongest growth globally, naturally healthy (NH) and fortified/functional (FF) compete for the leading position in terms of retail value sales.

NH, valued at $253 billion globally, has already outpaced FF. Consumers are more aware of what is included in the products than ever before and it is influencing purchase decisions as they look for minimally processed and more natural food and drinks in line with the clean label trend, which is boosting sales of NH.

More consumers like the idea of plant-based foods with intrinsic protein, mineral or vitamin content, with no need to artificially fortify them. They are increasingly looking for whole foods, ancient grains, green tea and plant-based proteins from nuts, seeds and pulses as well as ingredients with particular health functionality.

Adding botanicals to the list of ingredients is also a major trend, with preparations made from supergrains, superfruits or fungi rising in popularity in many food categories such as snacks, functional waters and hot drinks, among others. The use of jamun (black plum), moringa, goji berries, turmeric, maca and/or medicinal mushrooms like chaga are clear examples of this.

China has outpaced the U.S. in the NH category, with growth driven by natural mineral water, olive oil, 100 percent juice, high fiber noodles, nuts, seeds and trail mixes. Chinese consumers are showing increasing interest in these products due to rising income levels and health awareness, especially in first-tier cities.

Despite the NH categories driving health and wellness trends, FF products are still current, valued at $247 billion in 2017 globally. Although the U.S. is still the largest country, the category is mainly boosted by Asia Pacific and Eastern Europe, where consumers are looking for products with functional ingredients such as probiotics, omegas or vitamins as a means of minimizing nutritional gaps in their daily diet or to boost their well-being.