Consumers want brands to lead on mental and physical health

Editor’s note: Sam Killip is VP of insights at Attest. Attest is headquartered in New York and London.

It used to be enough for brands to stay in their lane. Sell the product, build the brand, avoid controversy. But in 2026, that line is getting blurry – with the political and economic landscape in turmoil, consumers are asking for more. Our latest research shows that Americans don’t just expect brands to deliver value. Increasingly, they expect them to show up on the issues that matter.

And those issues are deeply personal. Rising prices and economic stress remain the most pressing concerns, but mental and physical health are close behind. For many Americans, wellbeing isn't a personal matter anymore; it's a shared struggle, a structural failing and something they want the brands they trust to acknowledge.

Mental and physical health among top consumer worries

According to Attest’s 2026 U.S. consumer trends report (registration required), 25% of Americans cite mental health as a top personal concern for 2026, and 27% say the same about physical health. These concerns are outpacing others often associated with headline-making debate: AI (12%), immigration (11%) and even climate change (11%).

The age split is striking. Mental health is a top concern for 31% of both 18-24 and 35-44-year-olds, compared to just 16% of those ages 55-64. Physical health, on the other hand, follows the opposite pattern, rising steadily with age. For researchers, this duality reflects a generational divide not just in what people worry about, but in how they define wellness.

These concerns are also influenced by gender and income. Women are more likely to be concerned about both mental (27% vs. 23% of men) and physical health (31% vs. 24% of men), while lower-income respondents are significantly more likely to cite mental health as a top concern than higher earners (28% vs. 18%).

Despite demographic variation, health stands out as one of the most emotionally resonant consumer issues of the year. It’s a core quality-of-life concern that many feel the government has failed to address. And in the absence of strong policy action, consumers appear increasingly willing to transfer their expectations to the private sector.

Brands expected to influence and advocate

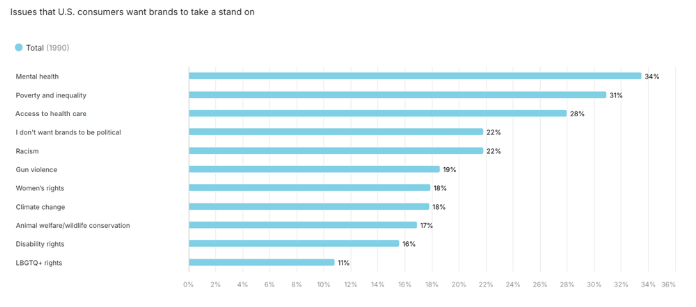

While mental health has historically been regarded as a private issue, it now ranks first as the topic consumers most want brands to take a stand on (34%). That places it above climate change (18%) and racism (22%) – two issues that often dominate brand-led social responsibility initiatives. A related issue, access to health care, is the third most important advocacy issue (28%).

Mental health is especially important to younger audiences. Among 18-24-year-olds, 43% want brands to take action on mental health, compared to just 27% of those ages 55-64. This generational divide signals a long-term cultural shift in expectations of what role brands should play in society.

This expectation also cuts across income and region. While lower-income consumers show slightly higher desire for brand action on mental health, it remains the top issue for Americans of all socioeconomic backgrounds (35% of lower earners vs. 32% of higher earners). And it emerges as the leading issue across regions, peaking with the Midwest at 36%.

Access to health care, too, maintains strong cross-demographic support, with 26% of lower earners and 30% of higher earners supporting brand involvement. Regionally, support is highest in the Northeast and West (30%), but even in the Midwest and South, it remains a strong priority. Meanwhile, campaigning on health care is slightly more popular among older Americans (support ranges from 26% of 18-24-year-olds to 30% of those over 45).

Combined, these two issues are redefining what it means for brands to be socially conscious. These are not abstract causes. They are daily lived experiences – and they are becoming a litmus test for brand relevance, especially in categories that touch on wellness, lifestyle or financial wellbeing.

What meaningful brand action could look like

For brands considering how to show up in this space, what matters most is to do it meaningfully. Tokenistic campaigns won’t cut it, and empty virtue signaling can do more harm than good. So, what does meaningful action look like?

Here are some examples:

- Headspace has built its entire brand around mental wellbeing, but it’s also collaborated with brands like Nike to integrate mindfulness into fitness.

- Sephora partnered with the Rare Impact Fund to expand youth access to mental health resources, blending beauty and wellbeing.

- Ben & Jerry’s regularly speaks out on health care issues, including access and equity, aligning its advocacy with its longstanding brand values.

- CVS Health made headlines in 2014 by removing tobacco from its shelves and has since invested in community health initiatives, positioning itself as a health care ally.

Smaller-scale actions can also resonate:

- Offering employees mental health days and sharing that policy publicly.

- Partnering with nonprofits to fund access to therapy or prescription services.

- Creating educational content that normalizes seeking help for mental health.

The key is relevance. If your brand's audience is already navigating these issues, supporting them with resources, visibility or advocacy makes strategic and human sense.

It’s also important to consider how this support is communicated. According to our data, 22% of Americans still prefer brands not to take a stand on political issues. That means any action on mental health or health care is best framed as access, empathy and care, rather than activism.

The takeaway for insights professionals

These findings highlight the growing role of consumer research in shaping brand positioning and corporate social responsibility strategy. This isn’t just about finding the right message – it’s about understanding what people need and what they’re asking from the brands they choose.

As mental health and health care rise on the list of consumer priorities, the opportunity for brands is twofold: to build relevance by aligning with these concerns and to build trust by acting in a way that feels sincere.

Methodology

All figures within this article are taken from research conducted on the Attest platform. The total sample size for the 2026 U.S. consumer trends report was 2,000 nationally representative working-age adults in the United States. The survey ran between November 17-20, 2025. The full report can be found here (registration required) and the research dashboard is available here.