Testing the connections

Editor's note: K.C. Boyce is vice president, Automotive & Mobility, and Energy, at Escalent. Nikki Stern is senior insights manager, Automotive & Mobility, at Escalent.

When our team at Escalent executed its second EVForward Brand DeepDive study in 2023, the goal was to provide a broader context for how vehicle ownership fits within consumers’ lives and how outside factors and preferences impact vehicle consideration.

Research studies are typically designed with a narrow focus in order to home in on attitudes to specific products or services. However, the world people live in is complex. Their personal ecosystem and the ways they view and use technology impact their purchase decisions – especially when investing in battery electric vehicles (BEVs). By widening the scope of our study to account for affinity for technology and charging brands, we aimed to develop a more accurate picture of consumer behavior.

With the entire ecosystem in mind, we approached this study with a wide lens, gathering input from a robust sample size on various topics, brands and attitudes in a quantitative setting. By building upon comparisons to our baseline research, we were able to dig deeper into how the market has changed.

Since our first EVForward Brand DeepDive study in 2021, the BEV industry has evolved significantly. At that time, legacy brands were beginning to release BEV offerings and EV specialist start-ups such as Rivian and Polestar were relatively unknown.

Today, the market has matured. Consumers are more familiar with EV specialist brands and the models offered by legacy automakers. More shoppers than ever are purchasing BEVs. With more products available, competition is higher. So are customer expectations.

To win over the next generation of BEV buyers, manufacturers will need to think beyond the in-vehicle experience and consider how a BEV fits into a consumer’s life and lifestyle.

Unpacking brand relationships

More than 1,500 new car buyers participated in the 2023 EVForward Brand DeepDive study. These included BEV owners, BEV intenders – meaning, consumers who are most likely to purchase a BEV as their next car based on proprietary propensity algorithms – consumers who are open to buying a BEV and consumers who are resistant to the idea.

We were particularly interested in the contrast between mainstream and luxury car owners, two groups who tend to have different expectations for their vehicles. As such, the study included about 500 luxury car owners and just more than 1,000 mainstream car owners. We examined attitudes toward 52 automotive brands, 12 public-charging brands and 11 technology brands.

EV specialists may be carving out a presence in the market but for now, new car buyers still prefer well-established automakers. Thirty-three percent of respondents said they would purchase from a well-established brand. Only 23% preferred an EV specialist brand, with the remainder being uncertain. This points to substantial opportunity for brands that are looking to expand their customer base.

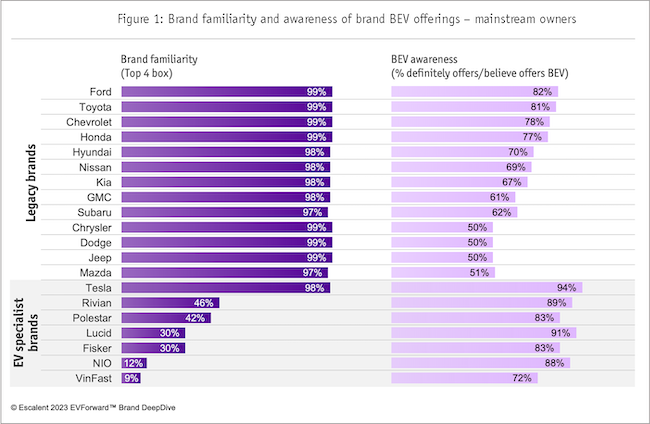

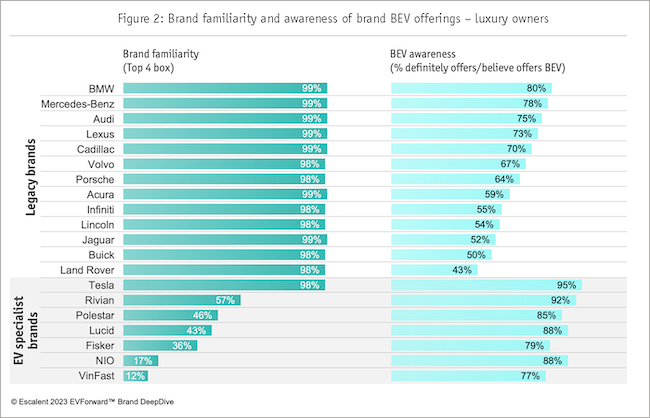

However, EV specialist brands hoping to boost sales must first increase consumer mindshare. Following this high-level question about participant attitudes toward established and emerging automakers, we examined awareness of specific brands and their BEV offerings. Among mainstream car owners, familiarity with legacy automakers such as Ford, Toyota and Chevrolet was at almost 100%. Similarly, luxury car owners conveyed near-universal familiarity with established brands such as Mercedes-Benz and BMW.

In contrast, most EV specialist brands, including Polestar, Lucid and Rivian, scored below 50% among mainstream car owners and below 60% among those in the luxury segment. Tesla was the exception. The EV pioneer scored 98% for familiarity among both luxury and mainstream car owners, placing it on par with legacy automakers.

Established brands lost some of their edge when new car buyers considered the brands’ EV-specific offerings. After indicating their familiarity with automakers, participants were then asked whether they thought each brand currently offered BEVs. Here, EV specialists fared better (Figure 1). Among mainstream vehicle owners, Tesla, Lucid and Rivian ranked the highest, with only one EV specialist falling behind their legacy peers.

Luxury car owners demonstrated an even stronger awareness of BEV models offered by EV specialists (Figure 2). Ninety-five percent said they thought Tesla offered a BEV and 92% said the same of Rivian, versus 80% for BMW, which had the highest recognition for BEV offerings among legacy brands.

Double-clicking on brand attributes

To better understand what would give one brand the edge over a competitor, we then examined which qualities consumers cared most about in a BEV and how these qualities were reflected in different brands.

For this section of the study, we first asked participants to rank the most important attributes of a BEV. Respondents were then prompted to apply the same set of attributes to specific automakers.

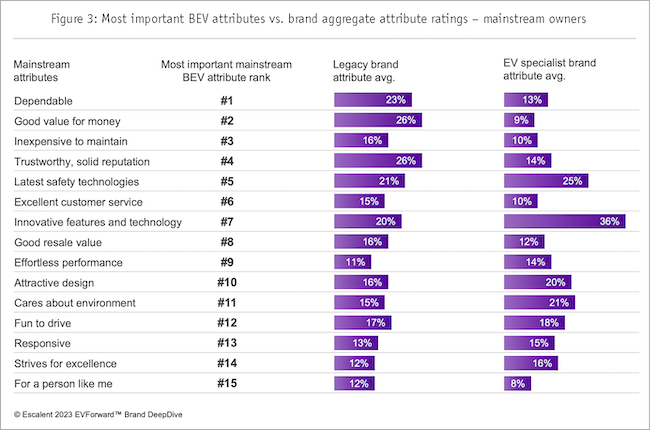

Mainstream and luxury vehicle owners agreed that, above all, a BEV should be dependable. When asked, 63% of mainstream vehicle owners ranked dependability as the most important attribute in a BEV, followed by “good value for money,” “inexpensive to maintain,” “trustworthy” and “equipped with the latest safety technologies.”

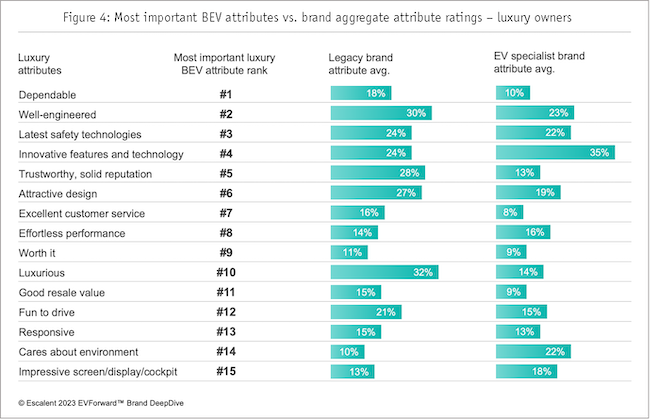

Luxury vehicle owners agreed on the latest safety technologies – which they ranked third – and trustworthiness, which came in fifth. Among luxury owners, though, “well-engineered” took second place, with “innovative features and technologies” rising to fourth.

These results are important because they demonstrate how a consumer will likely evaluate their next vehicle. The automakers perceived to be leading in these attributes can expect to gain a larger market share as more drivers opt for electric models.

We then aggregated attribute scores of specific automakers to arrive at an average score for legacy brands and EV specialists. The aggregated brand attribute scores revealed gaps between perceptions of legacy and EV specialist manufacturers. For instance, when asked to select attributes that describe legacy and EV specialist brands, an average of 23% of mainstream vehicle owners described legacy brands as dependable versus just 13% for EV specialist brands. In addition, legacy automakers scored higher for value for money, low maintenance cost and trustworthiness.

On the other hand, EV specialist brands performed better on technology-related attributes. An average of 25% of mainstream vehicle owners described EV specialists as having the “latest safety technologies” against a 21% average for legacy brands (Figure 3). The difference was even more marked on “innovative features and technology,” where EV specialists averaged a 36% rating versus 20% among legacy brands.

This pattern was also reflected among luxury vehicle owners. This group saw legacy brands as better in 11 of the 15 most important BEV attributes (Figure 4), including “dependable,” “well-engineered,” “latest safety technologies” and “trustworthiness.” However, an average of 35% of luxury owners described EV specialist brands as having “innovative features and technology,” while legacy brands netted just 24%.

This is a notable contrast and reveals an area where EV specialists could narrow the lead legacy automakers currently enjoy. We know that technology – and the broader ecosystem surrounding BEVs, including the charging network – is a key consumer focus. When vehicle owners think about their next BEV, they think about technology. As EV specialists continue building brand awareness, legacy brands must work hard to prove they can deliver on innovation.

Assessing the impact of brand media coverage

We also analyzed buyer sentiment toward legacy and EV specialist vehicle makers. As our initial brand dynamic findings demonstrated, Tesla boasts an enviable mindshare among consumers. It competed with legacy automakers for brand familiarity and outpaced every other brand for awareness of its BEV offerings.

The market disruptor also dominates the media cycle. Just more than half of survey respondents told us they had read or heard about BEVs in the past six months. Of that group, 70% of mainstream and 62% of luxury vehicle owners had seen news coverage about Tesla’s BEV offerings. All other brands received less than half of Tesla’s level of media recognition. Ford and Mercedes-Benz, the runners-up, netted around 30%.

That said, not all publicity is good publicity. When asked if they felt Tesla was moving in a positive or negative direction, approximately one in four new car buyers responded in the negative. The brand has received a flood of media attention in the last year and not all of it has been complimentary. Reactions from consumers suggest that, while the brand is on everybody’s mind, its media exposure could be a liability among buyers.

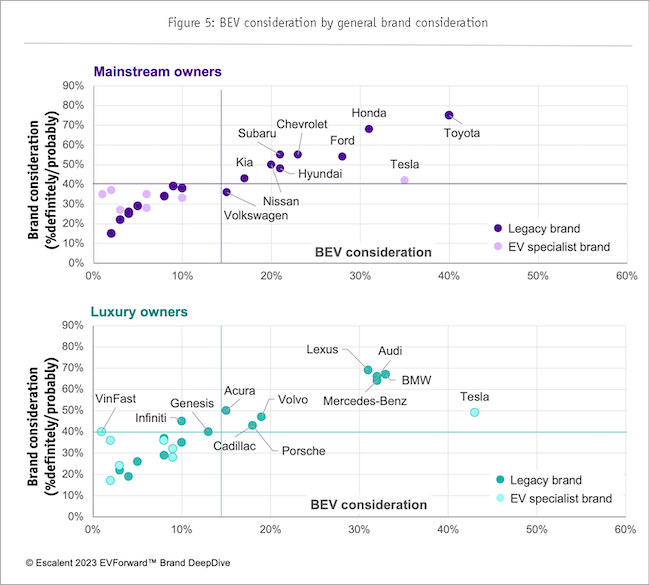

However, for now, the automaker is maintaining its edge. When weighing a BEV purchase, Tesla was the No. 1 brand luxury car owners said they would consider buying from and number two among mainstream car owners (Figure 5).

Since debuting its first BEV 15 years ago, Tesla has quickly built a reputation as a leader in the space. Our findings show that Tesla remains a formidable competitor for both legacy brands and start-ups. BEV-conscious consumers know the brand and its offerings. Moreover, the company has consistently invested in the ecosystem surrounding its vehicles. For example, Tesla announced that it would open its network of 12,000 nationwide North American Charging Standard connectors to partnering vehicle manufacturers.

Legacy automakers – especially those in the luxury segment – may find they can capitalize on Tesla’s declining brand sentiment to claim some of its market share. But to do so, they will have to produce products that meet or exceed Tesla’s use of innovative technology.

Considering the broader BEV charging ecosystem

Beyond perceptions of BEV-specific brands and attributes, we wanted to explore consumer relationships with technology and charging companies. Based on our prior research, we know that access to charging is top of mind for many consumers. Many prospective BEV buyers still harbor concerns about driving range, battery life and charge point coverage. As efforts to build out a national charging network accelerate, stories of slow and unreliable charging experiences have emerged in the media.

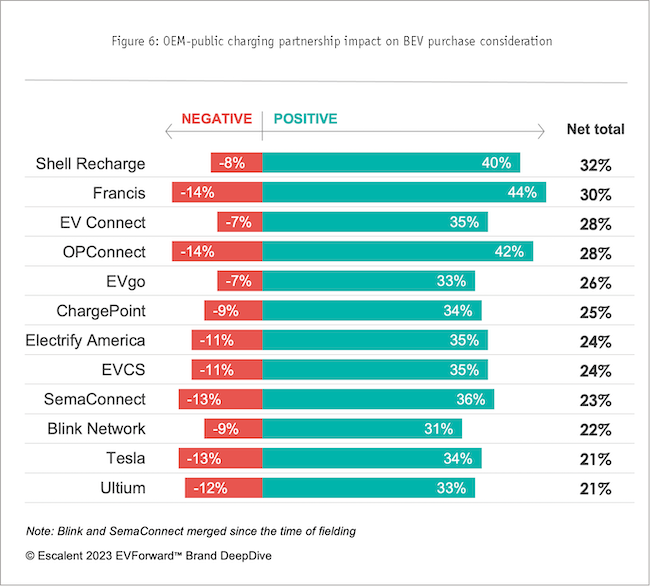

This study unpacked how familiar consumers were with different charge point operators (CPOs) and how a CPO-automaker partnership could influence consumer consideration to purchase a BEV from a particular automaker (Figure 6).

The majority of participants had limited knowledge of public charging infrastructure. Almost 80% said they knew little or nothing about public charging networks. Unsurprisingly, as consumers moved down the BEV purchase funnel, their awareness increased. Seventy-three percent of BEV owners said they had either used a public charging network in the past or knew a lot about public charging. Likewise, 80% of BEV intenders indicated strong familiarity.

When it came to brand recognition, consumers generally demonstrated low levels of familiarity and exposure to public charging networks. Tesla, again, was the exception. Almost 90% of respondents indicated that they knew of the Tesla Supercharger network. In comparison, only 34% said the same of second-place ChargePoint.

Despite a lack of familiarity with the brand landscape, our research pointed to a potential win for both CPOs and vehicle manufacturers. When participants were told that an automaker they favored would partner with a CPO, their likelihood of purchasing a BEV rose. This was true regardless of the charging brand.

On average, a partnership with a CPO would increase BEV consideration by 25%. BEV intenders demonstrated an even higher net positive impact. For automakers, this suggests that collaborating with any CPO could help improve EV sales. This could also enable charging networks to engage in some much-needed reputation-building.

That said, public charging is a relatively new frontier. The technology is still emerging, and many brands are troubleshooting reliability and access issues as they go. Automakers weighing CPO collaborations must ensure the CPO can offer their drivers a seamless and dependable BEV experience. A failure to deliver on that promise could result in adverse outcomes for both brands in the partnership.

Examining the strategic potential of technology

Unlike public charging networks, technology brands such as Apple, Amazon and Microsoft are well-known to consumers. Many have already made inroads into the automotive industry. Amazon is a major backer of EV start-up Rivian. Meanwhile, Honda and Sony announced the launch of their new joint venture at the beginning of 2023.

The last section of our study aimed to capture consumers’ feelings about 11 leading technology brands and explore the influence of partnerships between technology providers and automakers.

Unsurprisingly, almost all the technology brands included enjoyed near-universal familiarity. In addition, most had some visibility in the automotive industry. Those directly tied to transportation, such as Uber and Waymo, scored the highest for consumer awareness about brand involvement in the automotive space. Companies such as Apple and Google, which provide in-vehicle solutions such as mapping and routing, followed closely.

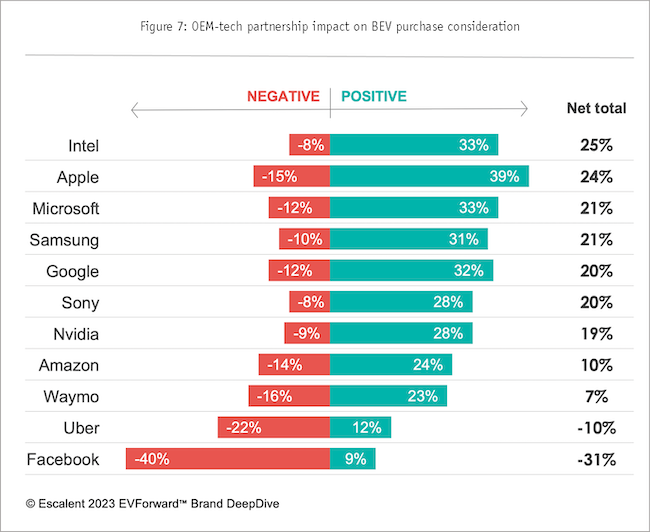

Overall, technology partnerships also positively impacted BEV consideration. However, our findings suggest that these collaborations require more careful consideration than those with CPOs. Participants noted that, in the majority of cases, were an automaker to partner with a technology brand on the design, production or features of a vehicle, it would make them more likely to purchase that BEV. For instance, a collaboration with Intel would increase BEV consideration by 25%. Two companies – Uber and Facebook – bucked this trend, scoring net negatives for BEV consideration (Figure 7).

This illustrates the need to consider the broader landscape consumers operate within when conducting research. We know that vehicle buyers appreciate technology and innovation. However, examining sentiment toward specific technology brands reveals that not all potential partners are equal. Automakers considering a strategic partnership with a technology brand could well find it helps establish or bolster their brand perceptions. But they must ensure they align themselves with a brand that resonates with consumers – and adds genuine value to their product.

Mapping an evolving BEV landscape

Brands and consumers are leaning into the growing BEV market. Awareness of offerings is rising. Meanwhile, ambitious goals set by federal and state governing bodies – along with private companies – are catalyzing investment. Legacy brands may benefit from latent brand strength, but with EV specialists leading on technology, an influx of sales in the coming year could allow any proactive player to expand its market share. Conversely, automakers that fail to convince customers of their capacity for innovation are at risk of losing ground.

As such, recognizing the needs and expectations of tomorrow’s vehicle buyers has never been more crucial. Part of what we set out to understand in the EVForward Brand DeepDive was what motivates consumer behavior. The more researchers can capture people’s nuances and complexities, the better the results will be. By using a broad scope to survey the brand landscape specific and peripheral to BEVs, we uncovered a more comprehensive picture of what vehicle shoppers will be looking for in the future.

Consumers have affinities for certain technology brands. For automakers looking to stand apart from the competition – and, particularly, emerging brands that don’t have the advantage of a halo effect – a strategic partnership with a trusted technology brand could help their offering rise above the noise.

As consumers navigate the shift to BEVs, they will also need to get comfortable with a new network of charging infrastructure. By helping to build out services around BEVs – either through a proprietary network or a partnership with an existing CPO – automakers can help make that journey smoother.

Consumers’ lives are increasingly impacted and powered by technology. To capture the attention and loyalty of vehicle shoppers, brands must ensure that their BEVs fit seamlessly into the ecosystem of applications and solutions surrounding them. Delivering on that promise will require researchers and manufacturers to develop an in-depth understanding of the brands and attributes their customers value most.